2024 Outlook: Weaker Population Growth + Strong Housing Supply = Rental Market ?

[PAID CONTENT SAMPLE] Overview of important developments in the Toronto Metro housing market and macro reported in January 2024

10 Best Charts of 2023

Before diving into the current newsletter, please take a moment to explore my compilation of the top 10 charts from 2023. This concise and insightful post won’t be sent by email. (link)

Highlights

The Toronto Metro resale market strengthened further in January, while the rental market remained stable.

Additional policies were introduced restricting international students.

Population growth is expected to slow down significantly in 2024.

Strong housing completions were observed in 2023, with a similar level anticipated for 2024.

There was a divergence between higher-priced and lower-priced rentals in 2023.

The rental market is expected to weaken in 2024 but there is a lot of uncertainty.

Real Estate Market

In the current newsletter, I'd like to highlight a few important dynamics, therefore, the overview of the real estate market will be very brief. The resale market continued to strengthen in January, while the rental market remained stable and balanced.

There was a noticeable uptick in new listings and while it lacks significance when properly adjusted for seasonality, it deserves closer attention. Prices continued to decline but are expected to stabilize in the near term.

Population Growth

Significant changes related to international students were announced by the Canadian Government in January (link1, link2). Here are a few key points:

The number of study permits will be capped for two years with a limit of about 360,000 set for 2024, representing a roughly 35% reduction from 2023 levels. Different quotas will be set for different provinces, with Ontario facing a reduction of 50% or more.

New enrollments in public-private partnership college programs will no longer be eligible for the Post-Graduation Work Permit (PGWP).

Spouses and common-law partners of new international students will no longer be eligible for open work permits, except for graduate (master’s and doctorate) and professional degree-granting programs.

These changes, coupled with earlier policies such as the reinstatement of a 20-hour-per-week work limit and the elimination of PGWP extensions (link), are expected to have a significant impact.

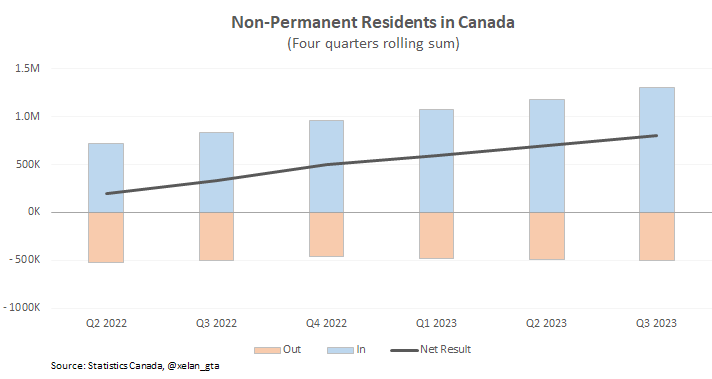

However, before discussing the impact of the new policies it’s crucial to clarify how non-permanent residents contribute to population growth. While new permanent residents add to it, non-permanent residents continuously arrive and leave Canada, boosting population growth only if inflows exceed outflows.

Over the last four quarters, inflows have exceeded outflows by over 800,000, contributing the same amount to population growth in Canada. However, every non-permanent resident has an expiry date on their status, which means record inflows will lead to record permit expiries down the road. The only way for non-permanent residents to settle in Canada is by obtaining a Permanent Residency (PR).

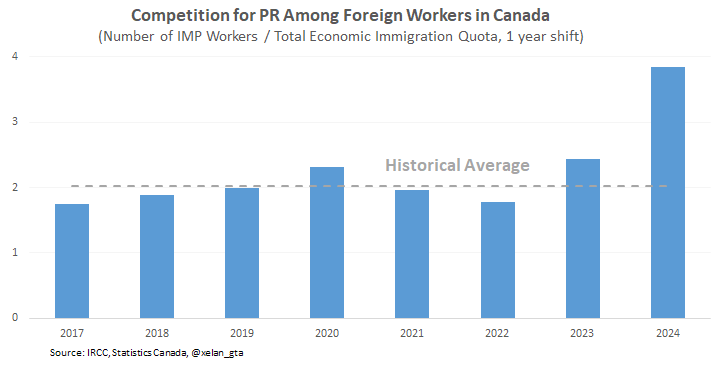

Since the quota for PR is limited and announced well in advance, competition for PR can be estimated by comparing the total number of International Mobility Program (IMP) permit holders, mainly linked to former international students, to the total Economic Immigration quota. Data reveals that competition skyrocketed this year, nearly doubling compared to the historical average.

Without extensions, those who fail to obtain PR in time will be required to leave Canada. Reverting to the historical average would require a reduction in the pool of IMP temporary workers by about 475,000, deducting the same amount from population growth.

But that’s not all, Canada also experienced a record inflow of international students in 2023. It will take time for them to complete their studies and gain work experience before applying for PR, resulting in an estimated 3-year delay. A record number of international students who enrolled in 2023 are anticipated to apply for PR around 2026 leading to higher competition in the future.

The number of international students per immigration spot announced for 2026 is about 50% higher than the historical average. Reversion to the mean would require the pool of international students to shrink by about 330,000 by 2027.

In summary, the sustainable conversion of non-permanent residents to PR in Canada, based on its immigration capacity, will require a reduction of approximately 800,000 from the pool of temporary workers (IMP) and international students by 2027, deducting an equivalent amount from population growth.

That is the mistake many people are making. They are counting only inflows but completely overlook outflows.

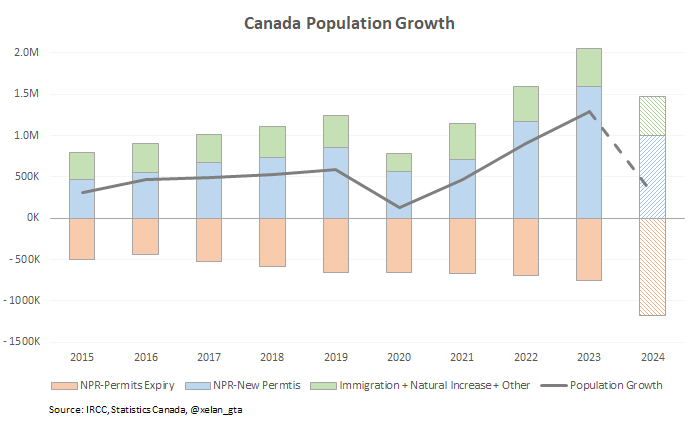

2022 was a very strong year for non-permanent inflows. If we assume 2024 inflows to be around that level, a reasonable projection leads to a substantial decline in population growth to 300,000 despite strong inflows and record immigration. This is due to increased outflows.

These outflows result from various factors, including the termination of PGWP extensions and the normal expiry of a record number of permits issued in previous years.

While this model is based on reasonable assumptions, there are a lot of uncertainties regarding future inflows and outflows. Factors such as lower-than-expected international student admissions or expired permit holders choosing to remain in Canada illegally could impact these projections. Additionally, new government policies may further influence these flows. It’s important to note that this modelling doesn’t assume any economic slowdown or deterioration in the labour market; such occurrences would likely result in even lower population growth.

Furthermore, population growth declines will most certainly have a more pronounced effect on the Toronto Metro area due to its higher concentration of non-permanent residents and population outflow components to other cities and provinces in Canada.

Regarding timing, the latest input data remains robust, so the upcoming Q4 2023 population growth data is expected to be strong, potentially setting a new record.

Q1 2024 could also show strength due to the arrival of international students and CUAET applicants, though some outflows may begin during this period. A noticeable population growth decline is anticipated in Q2 2024 data and beyond.

Housing Construction

In 2023, housing construction in Toronto Metro witnessed significant activity, with the number of housing units that began construction ranking the second-highest in the last 30 years.

Concurrently, housing completions reached the third-highest level during the same period.

Although housing starts are anticipated to decrease in 2024 due to sluggish sales in 2022-2023,

they are not expected to materially impact completions until 2027 due to a large share of apartments with a long construction cycle. Moreover, there is currently a record number of units under construction, ensuring a robust housing supply in the coming years.

Overall, completions in 2024 are expected to remain in line with those in 2023. However, apartment completions which include both condos and rental apartments are expected to increase further. The model is not very accurate though.

Urbanation, one of the leading analytical agencies, is also expecting an increase in 2024 condo completions.

Rental Market

Despite record population growth, the Toronto Metro rental market surprisingly weakened in 2023. While more data on this topic emerged recently and further insights are anticipated, overall statistics regarding the rental market are less than ideal. It's worth noting that different sources analyze only subsets of the market, excluding units transacted on platforms like Kijiji or housing arrangements involving multiple international students in basement apartments, which are not covered by any statistics. Typically, I focus on the rental market based on transactions reported by TRREB in my newsletters and refer to it as “Toronto Metro rental market”.

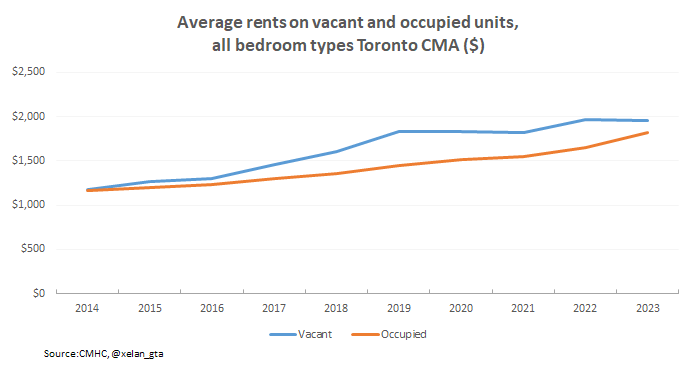

CMHC, for example, focuses primarily on purpose-built rental buildings, providing insight into a different share of the rental market. Key findings from their newly released data include a significant discrepancy between higher-priced and lower-priced apartment rents. For instance, there was a notable increase in vacancy rates in newer rental buildings constructed after 2015, while overall apartment vacancies declined, tightening the apartment rental market in Toronto Metro.

Although the average rent for vacant units remained relatively unchanged in 2023, the average rent for occupier units increased substantially,

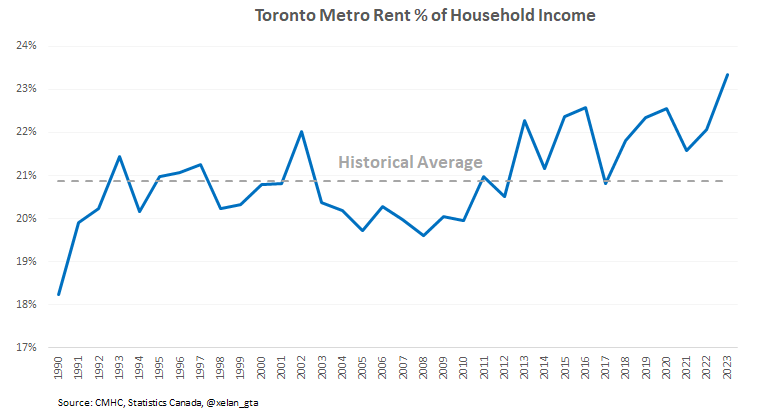

making it the most unaffordable rental market on record since the data exists.

This suggests that rental affordability is undoubtedly part of the story, though it's not yet clear how the balance between rental supply and demand played out in 2023. For example, new data revealed that the share of rental units among all condos in Toronto Metro grew from 36.6% to 38.4% in 2023, effectively adding 8,647 units to the rental market on top of the high number of new units completed that year.

Despite these insights, there are still many unknowns. For instance, 2023 population growth data for Toronto is not yet available. Without a full understanding of the reasons behind the resilience of the Toronto Metro condo rental market in 2023, it would be difficult to set accurate expectations for 2024.

Conclusions

Toronto Metro real estate market continued to tighten in January and the rental market remained stable. Despite further price declines, stabilization is anticipated as early as next month due to a stronger market balance and seasonality.

The overview of the real estate market in this newsletter was brief, as the primary focus was on exploring the important dynamics between population growth, housing construction, and the rental market, aiming to set reasonable expectations for 2024. These dynamics are crucial for the overall Toronto Metro real estate market.

Significant new changes related to international students were introduced by the government in January. Most notable of those include caps on international student admissions, limitations related to obtaining PGWP, and work opportunities for accompanying partners.

Due to new government regulations, a natural cycle of non-permanent resident permit expiry, and other factors population growth in Canada is expected to decline. Between Q2 2024 and Q2 2025, it could easily reduce by half or more from the current level of 1.25 million. This decline is attributed to both a decrease in inflows and an increase in outflows, which is often overlooked.

As I mentioned in one of my Twitter posts:

“The dynamics within the non-permanent residents group resemble waves in the ocean. The larger the wave hitting the shore the bigger the outflow follows.” (link)

This is due to the expiry of permits and the limited capacity of the immigration system. Only temporary residents absorbed by the immigration system will settle in Canada; the rest will have to leave after their temporary status expires.

Can these outflows be reduced? Potentially, but current options are limited. Increasing immigration targets or extending the temporary status of non-permanent residents are off the table due to recent policy changes. Allocating a higher share of immigration to non-permanent residents within Canada will help to prevent outflows but wouldn't impact resulting population growth. Given the current policies, public opinion, and political climate, I see no viable options to impact population growth by preventing non-permanent resident outflows.

An increase in outflows in 2024 would have occurred naturally, and recent government policies such as the termination of PGWP extensions will amplify those outflows. Other policies such as higher income requirements and eligibility limitations for PGWP and spousal work permits should additionally lead to a decline in inflows. While loopholes may be found around some policies, such as capital requirements, circumventing policies like PGWP extensions and student caps would be challenging. Overall, I believe, new policies can be quite impactful.

Meanwhile, housing completions are expected to remain strong. Last year marked the third-highest completion rate in the last 30 years, and 2024 is expected to see similarly high numbers.

Considering the anticipated decline in population growth and robust housing completions anticipated in 2024, it’s interesting to see how the Toronto Metro rental market will evolve. It is challenging to properly answer this question due to limited data availability and significant reporting delays. If the rental market didn’t tighten during the population boom in 2023 it may not slow down if population growth declines in 2024. However, the base case suggests a weakening Toronto Metro rental market, especially considering that it's the most unaffordable on record. Potentially this weakening can be quite significant but there is a lot of uncertainty at the moment.

Note: The article was modified from the original version on Feb 10, 2024, to correct a few mistakes related to inconsistencies and omissions. It was also modified on Apr 5 to include Urbanantion’s forecast regarding 2024 condo completions.