A Turning Point for Toronto Real Estate Market?

A Turning Point for Toronto Real Estate Market?

Overview of important developments in the Toronto Metro housing market and macro reported in February 2022

Resale Market

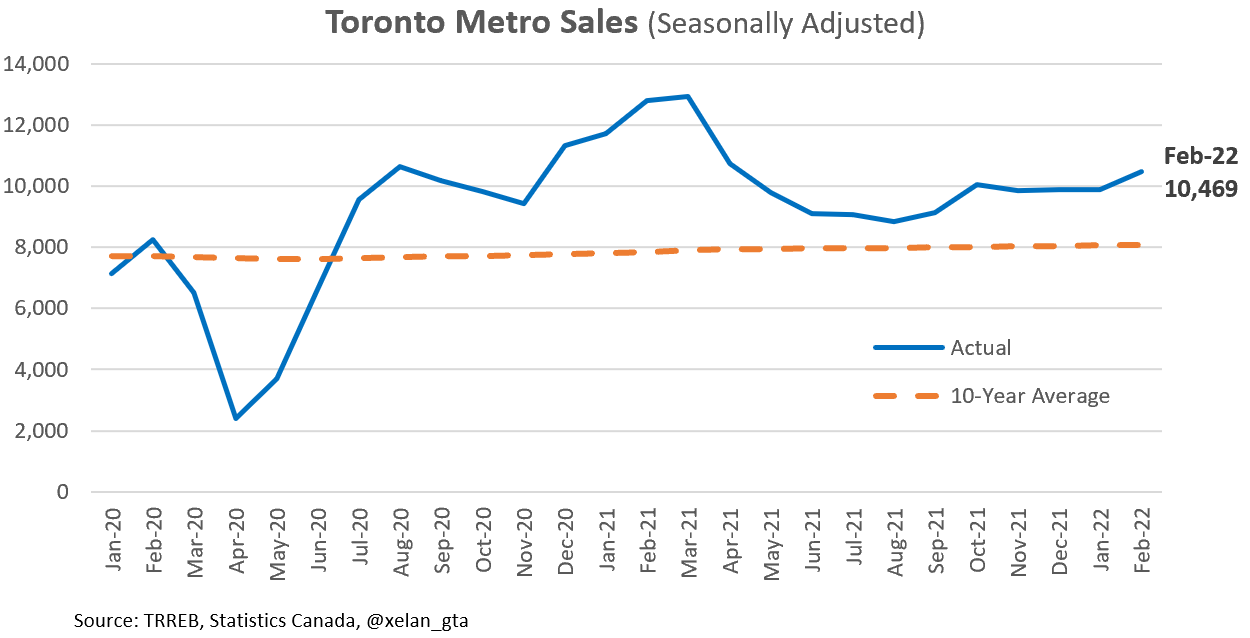

Toronto Metro Real estate market was exceptionally strong in February, several new records were set, and based on the vast majority of metrics, 2021-2022 market performance and strength are eclipsing those from 2016-2017.

Sales continue to be strong rising to 30% above the 10-year average.

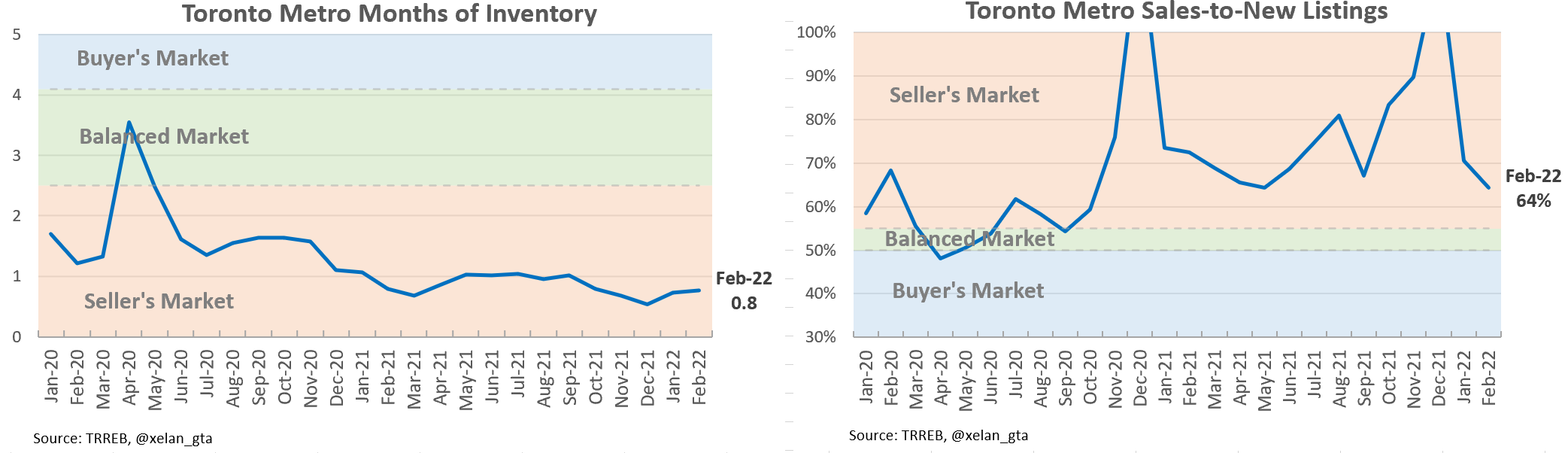

Market balance indicators remain very tight. Both of them weakened a little in February but still remain very deep in the seller’s territory suggesting further price growth in the near term.

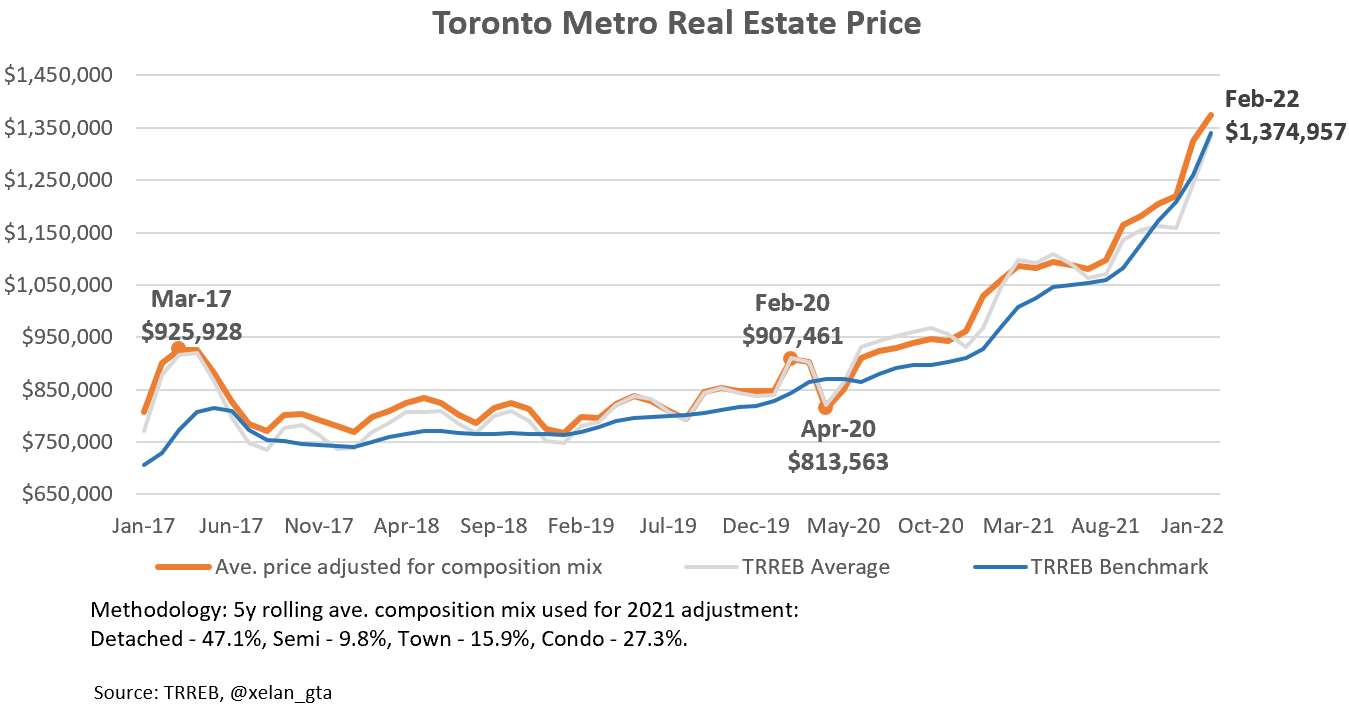

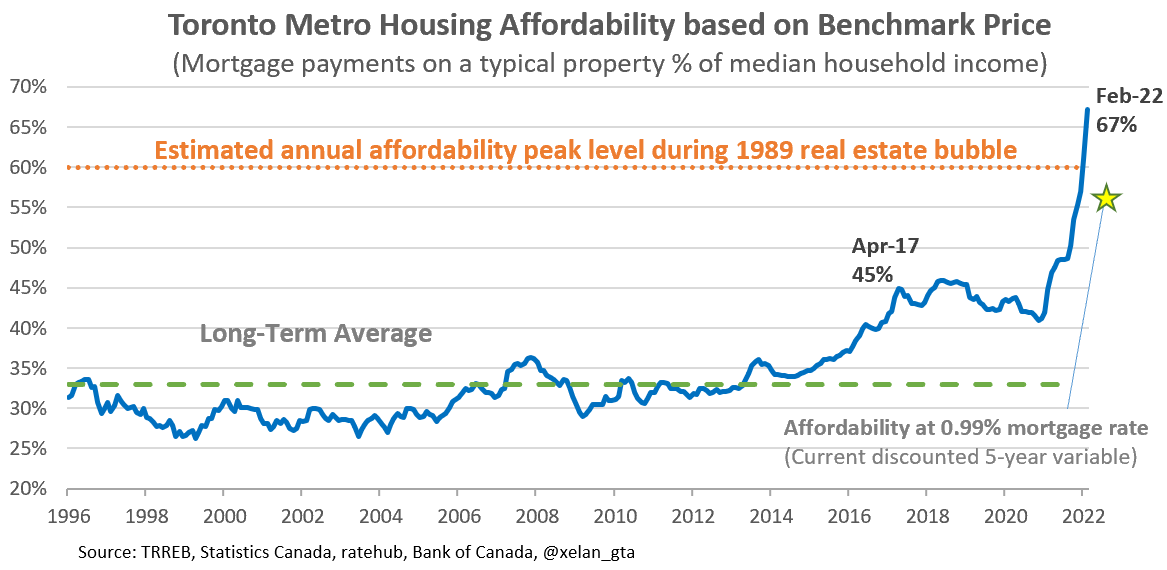

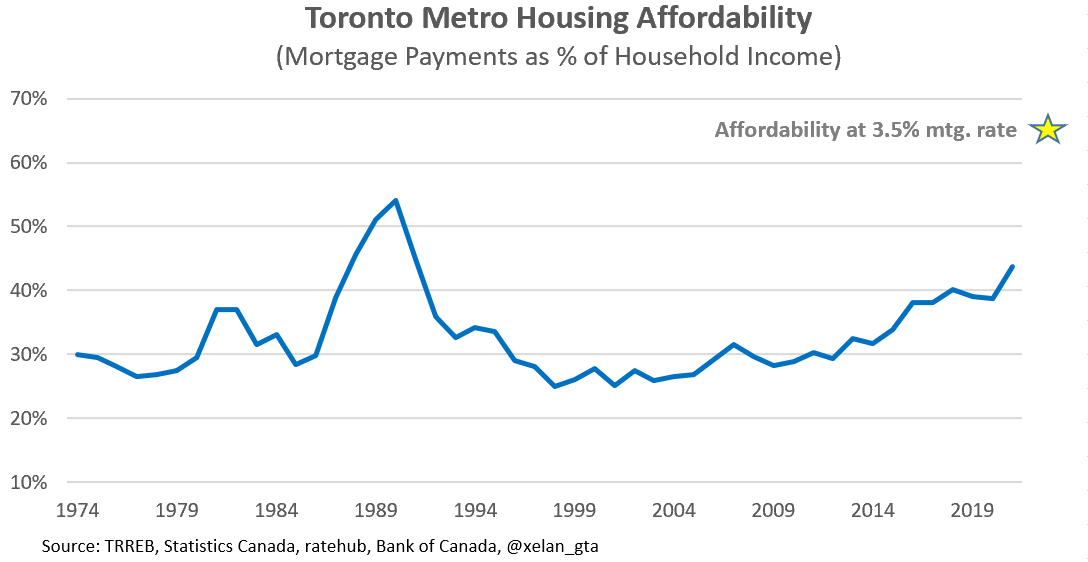

As s result of the tight market prices continue to grow rapidly in a hockey stick pattern.

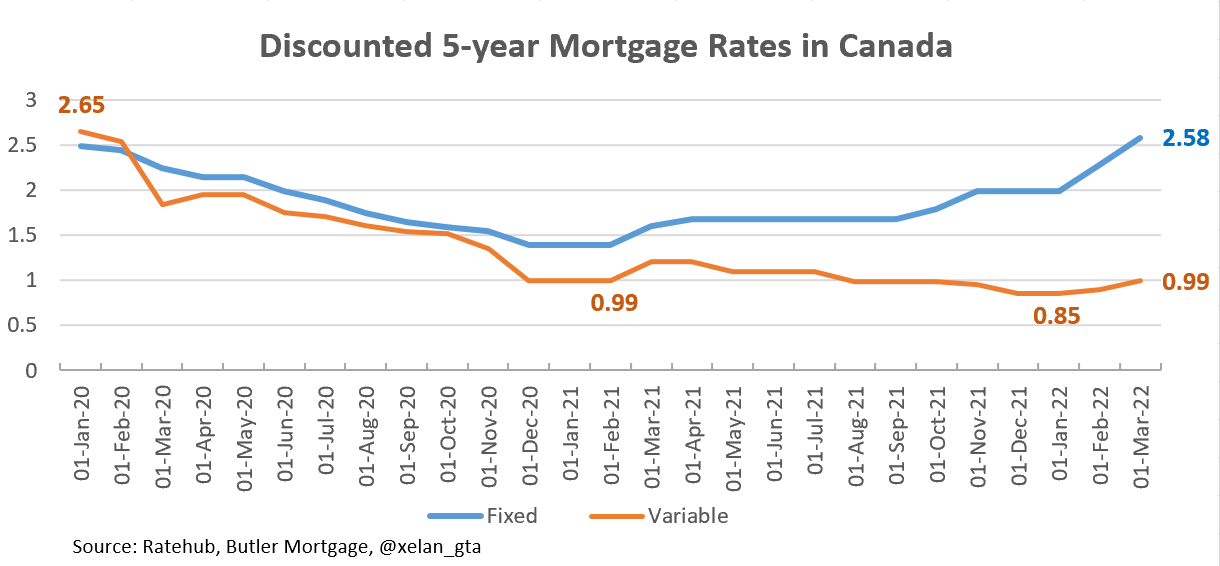

This is happening when fixed mortgage rates continue to rise.

The rise of the mortgage rates and prices at the same time squeezes housing affordability from two sides sending it to an unprecedented level.

If Toronto Metro real estate market is going to face a correction I believe this chart will be seen as one of the clear warning signs. Important to note that while the affordability metric shows major imbalance and risk, it can’t predict the future and there are options available to improve affordability without price correction.

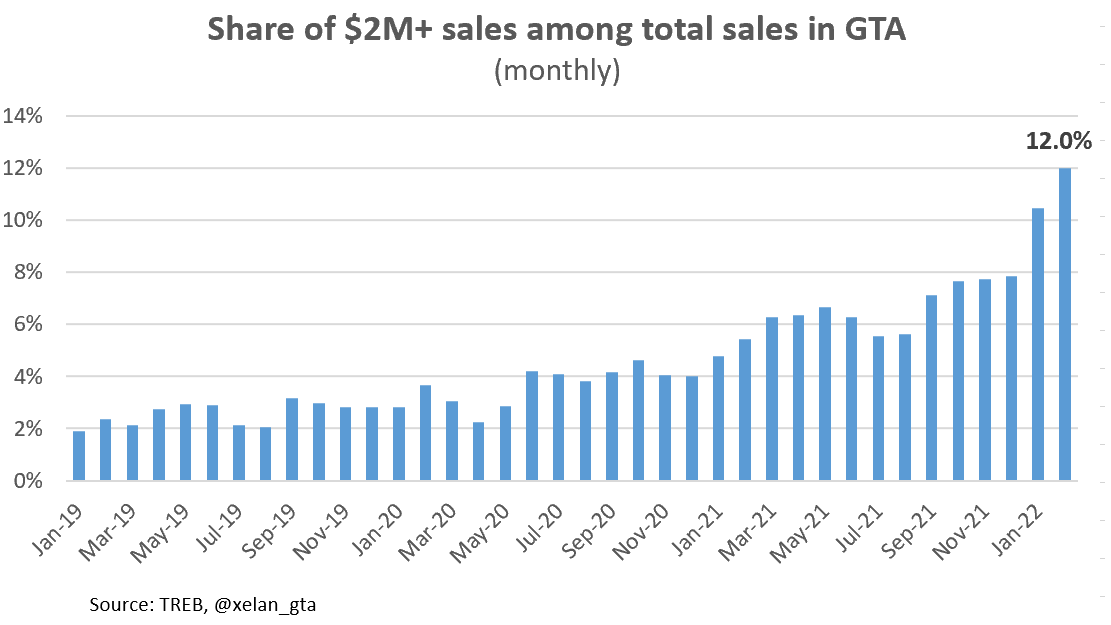

In February Toronto Metro reinforced the title of the most expensive metro market in Canada and the price gap between Toronto and Vancouver metro areas widened from 0.4% to 2%. Within Toronto Metro, the condo sector was stronger than single-family and expected to outperform going forward. Share of luxury sales ($2M+) increased further to 12%.

Investment

Switching from homebuyers to investors reveals another emerging risk. Rising rent prices are unable to offset rapidly growing condo prices coupled with increases in mortgage rates. As a result cash flows for the new investors are falling quickly.

Condo cash flow, where principal payments are excluded (as a form of savings) declined substantially below the historical average. This is an absolutely new risk, which wasn’t present in the market since the series start in 2012.

Toronto Metro real estate market is becoming exceptionally unaffordable not only for homebuyers but also unattractive for investors as well, which is also confirmed by other investment metrics. It’s very hard to see how the current level of demand continues unless attractiveness improves.

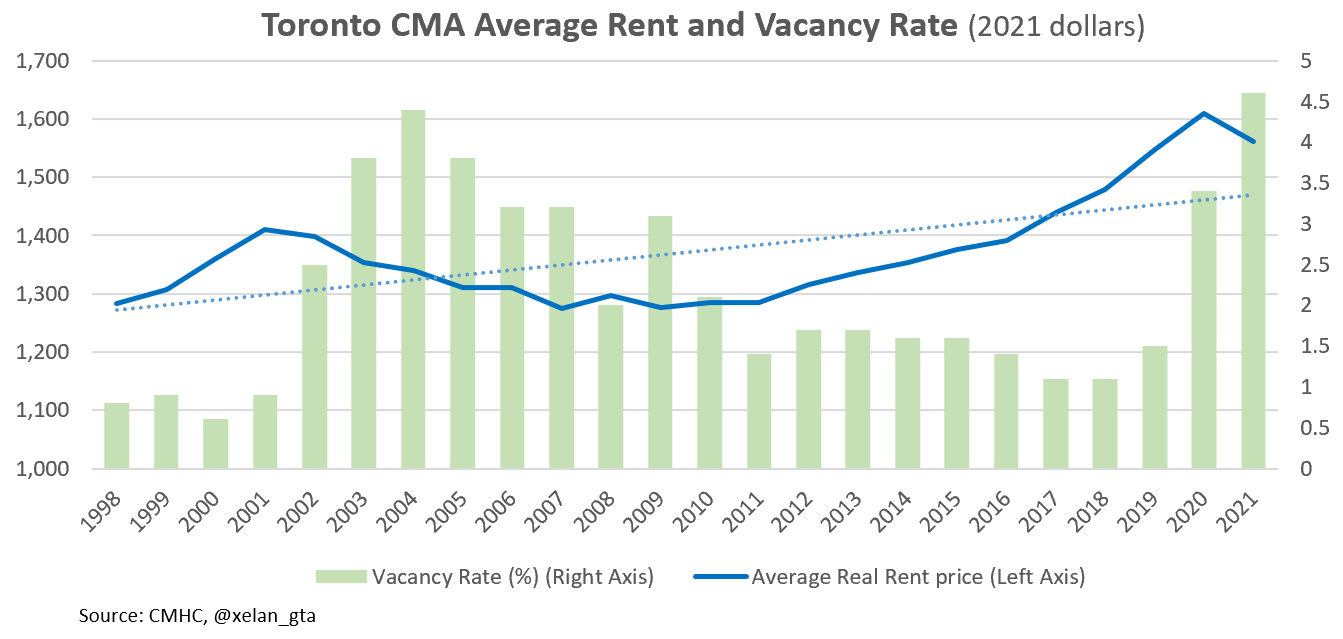

Rental Market

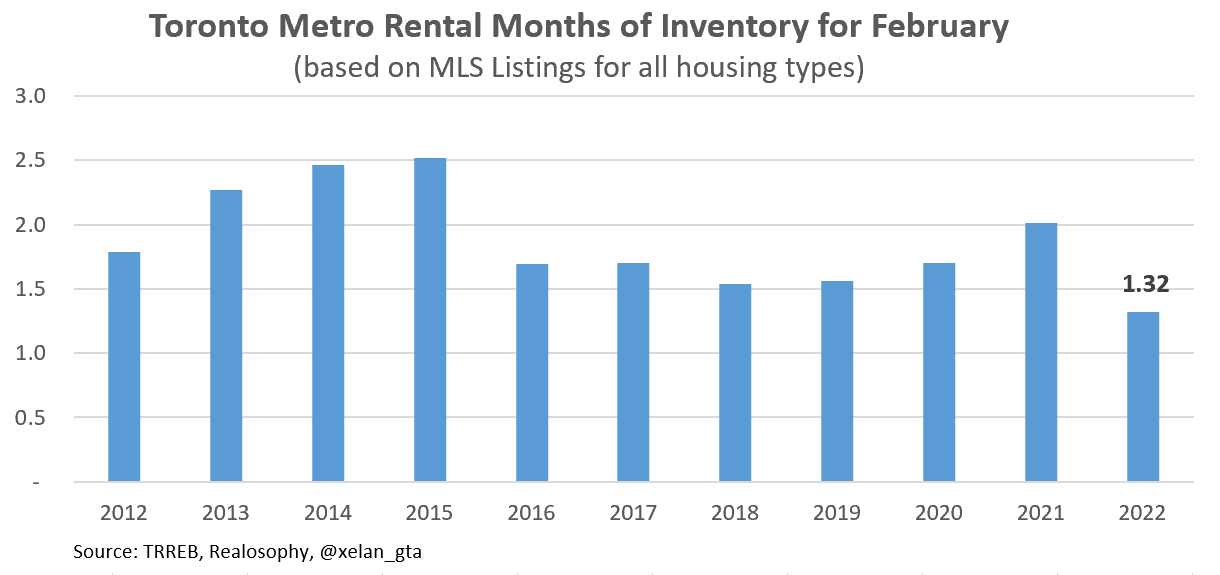

Rental Market is strong and facing upside risks. Market balance is the tightest since at least 2012

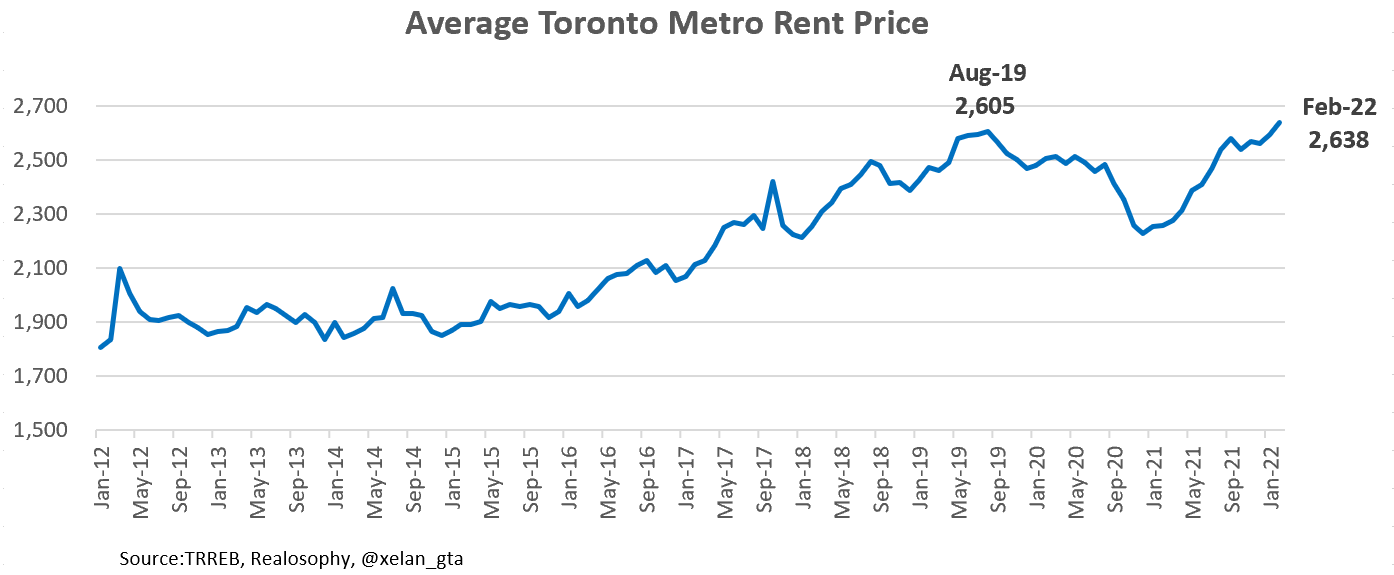

Rent prices growth was moderate recently due to the slow seasonality. It is starting to pick up.

CMHC released data for the purpose-built rental market. It reveals that the vacancy rate in 2021 was a record high within the whole series. High vacancy translates into about 10,000 of extra vacant rental units compared to 2019.

Rental market statistics are captured by CMHC in September so the rental market definitely improved since then however it still remains being a tale of two rental markets where condo rentals are much stronger than purpose-built ones. It’s important to keep an eye on both of them for a full picture of the rental market.

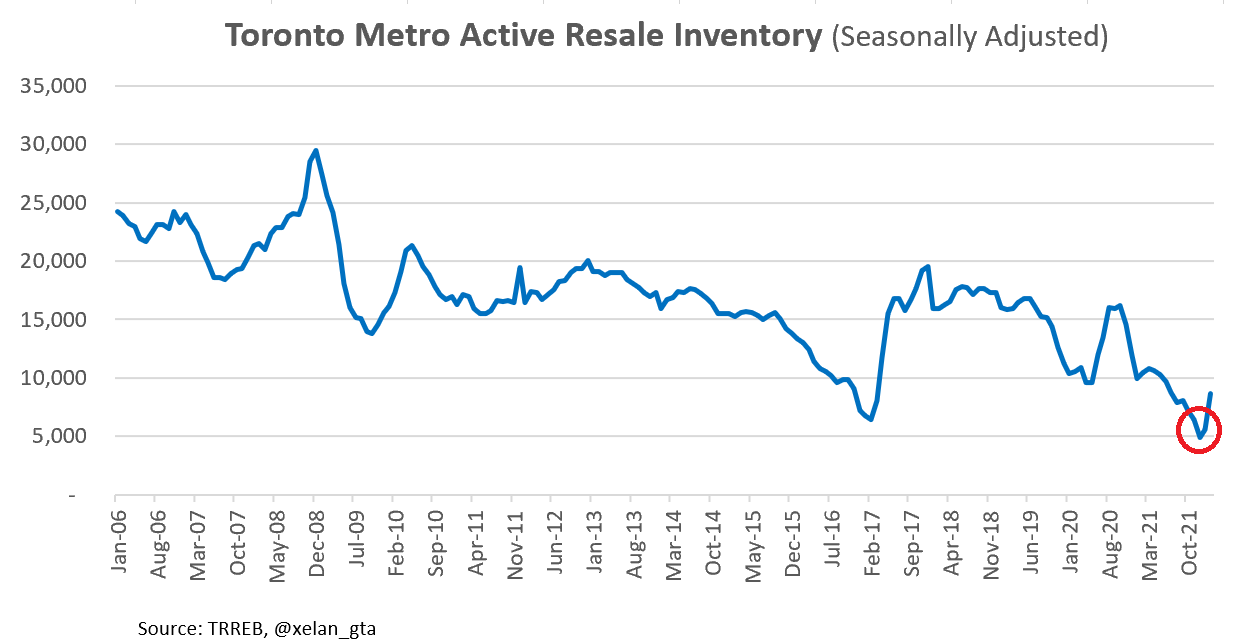

Turning Point

Here is the chart which illustrates the best turning point I’m referring to.

Data is quite volatile so it’s not obvious yet from the chart if that’s just a temporary bump or trend reversal. The weakening of the market balance indicators and macro picture make me think that reversal is a more likely scenario here.

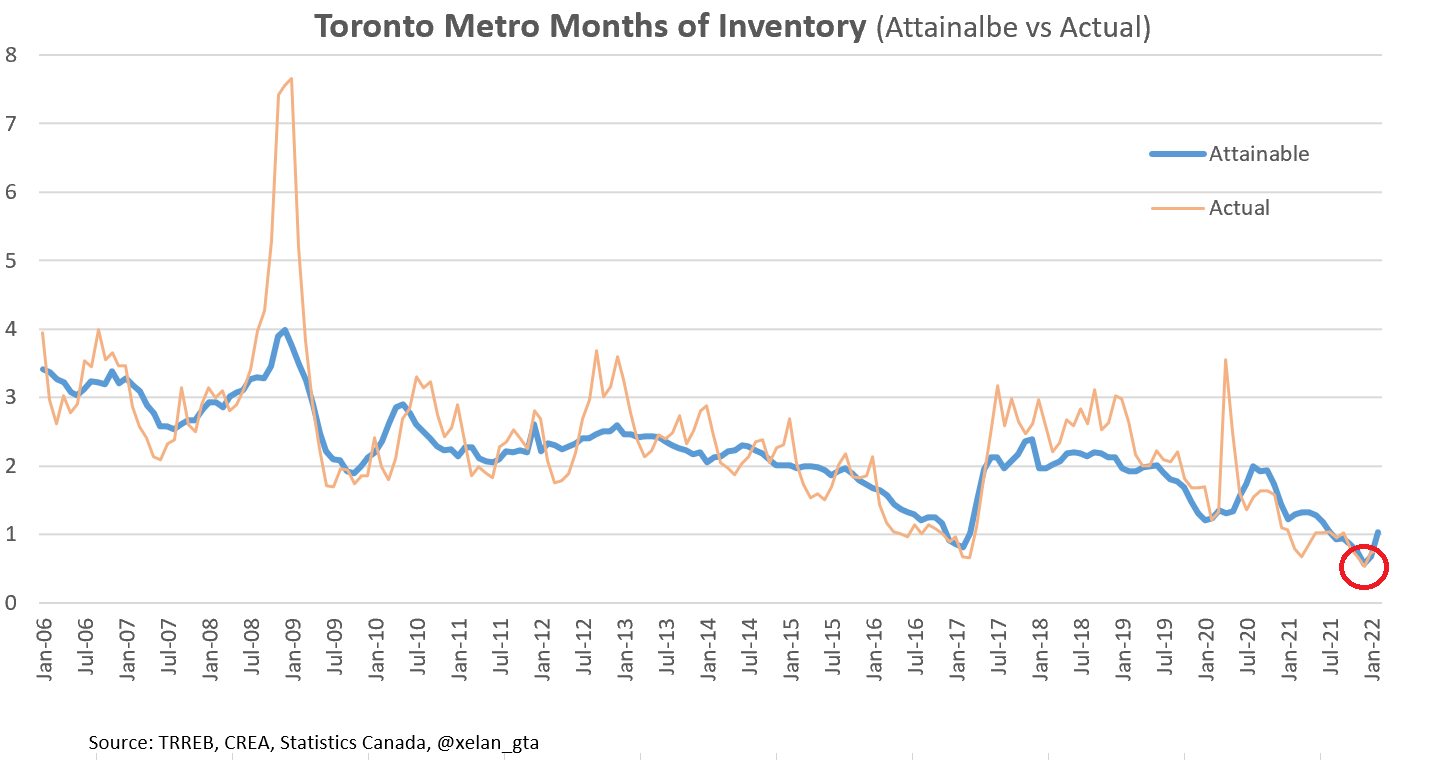

Here is the chart for one of the market balance indicators - Month of Inventory along with the calculated attainable value showing a potential turning point as well.

Why do I think the market is at a turning point?

I don’t want to go too much into details behind reasoning but will say that the primary reason behind new listings increase in my view is related to the expectation of the higher interest rates.

And resulting consequences for housing affordability and real estate investment attractiveness.

Data in the coming months will define if my thinking is correct. A decline in sales coupled with increase in new listings would be a strong evidence of the price growth expectation change.

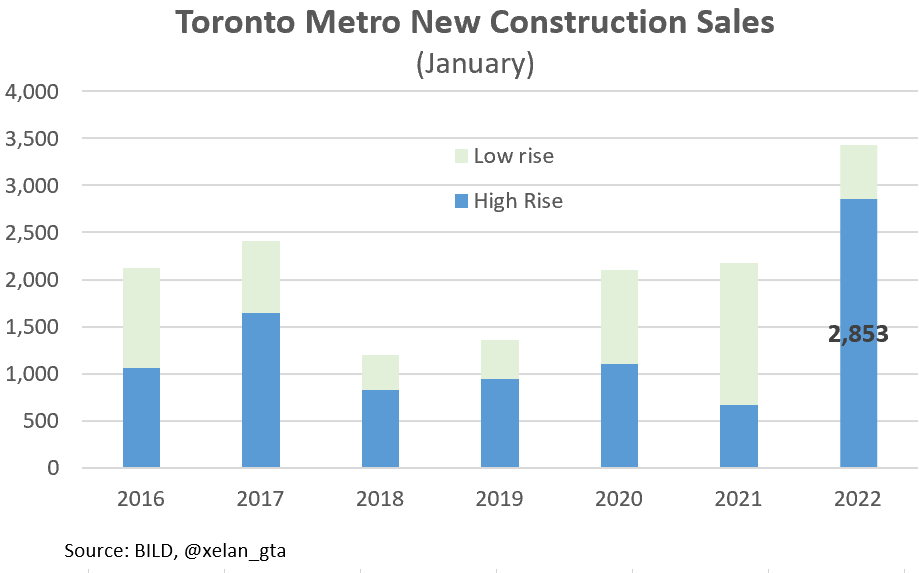

New Construction

New construction sales were exceptionally strong in January, thanks to the condo sector.

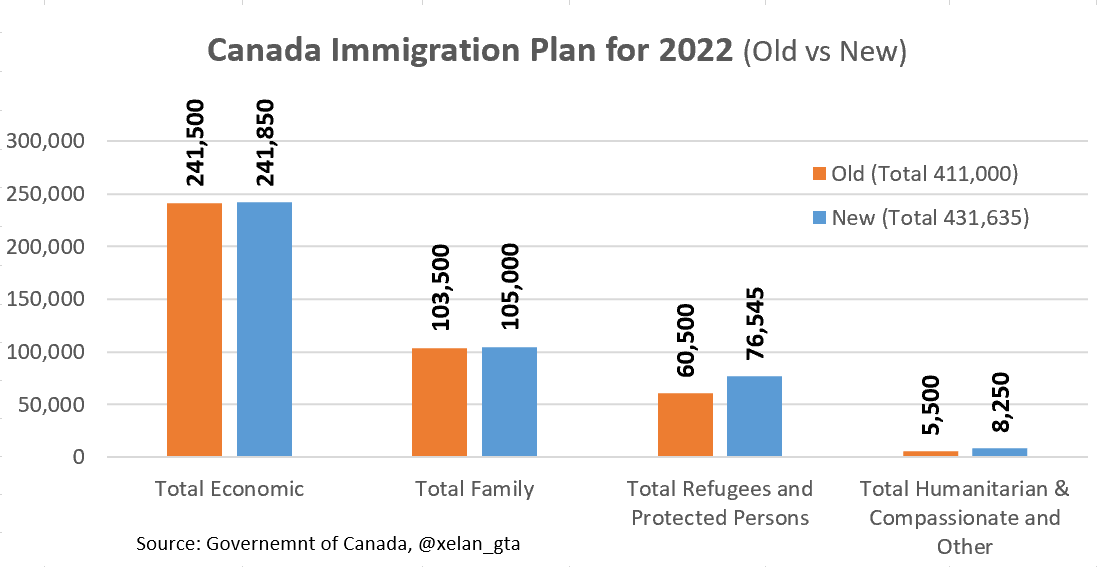

Immigration and Census

Canada announced that it will be further increasing immigration targets for 2022-2023 years compared to the previous planning done in 2020. The target increased from 411,000 to 431,645 for 2022 and from 421,000 to 447,055 for 2023. The target for 2024 is set as 451,000

The vast majority of the increase this year is attributed to refugees and humanitarian categories.

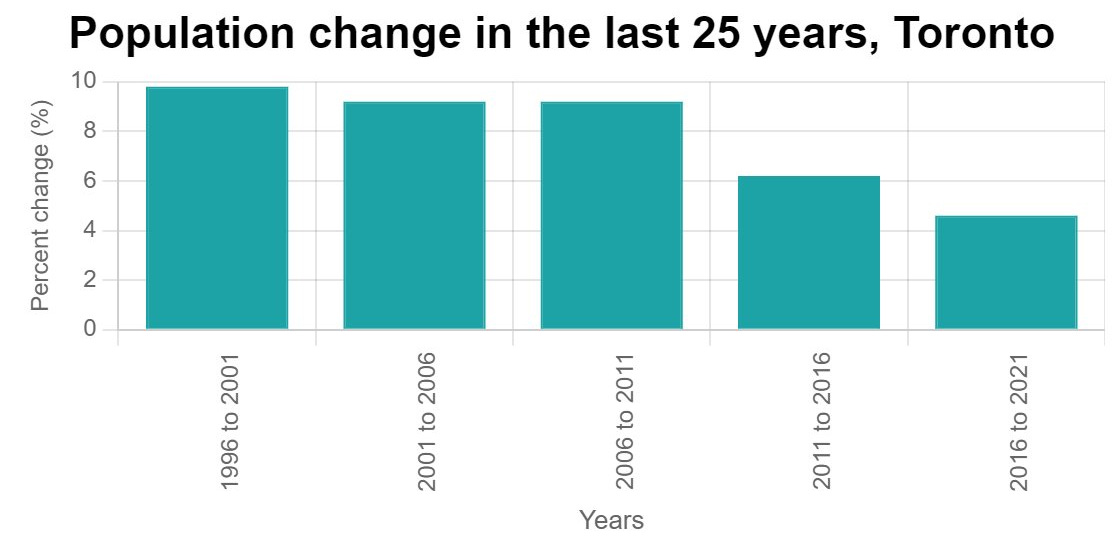

Population and housing data from Census 2021 was released in February as well. It revealed several interesting trends:

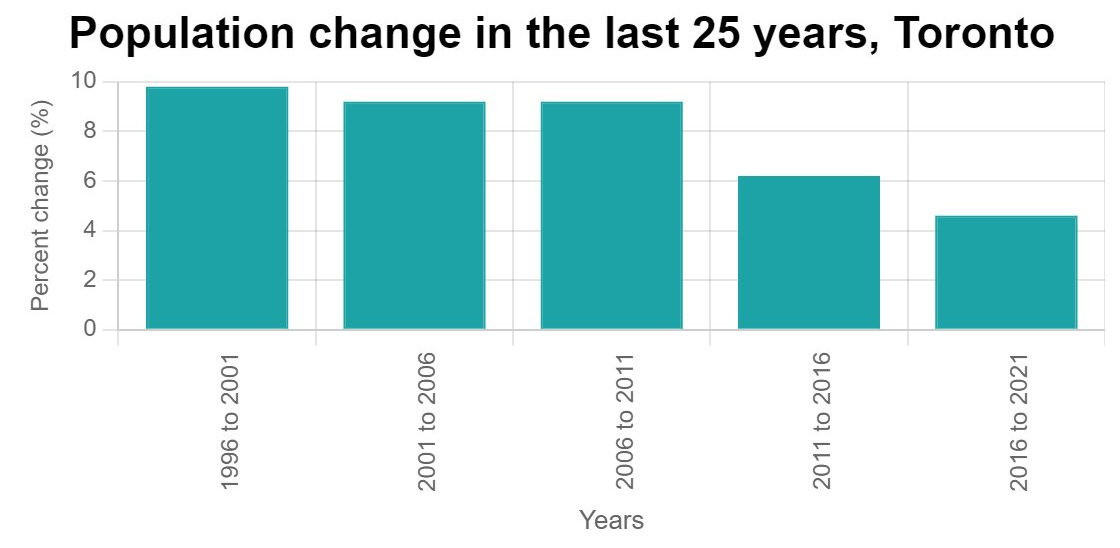

Toronto CMA population growth is slowing down even during 2016-2021 population boom.

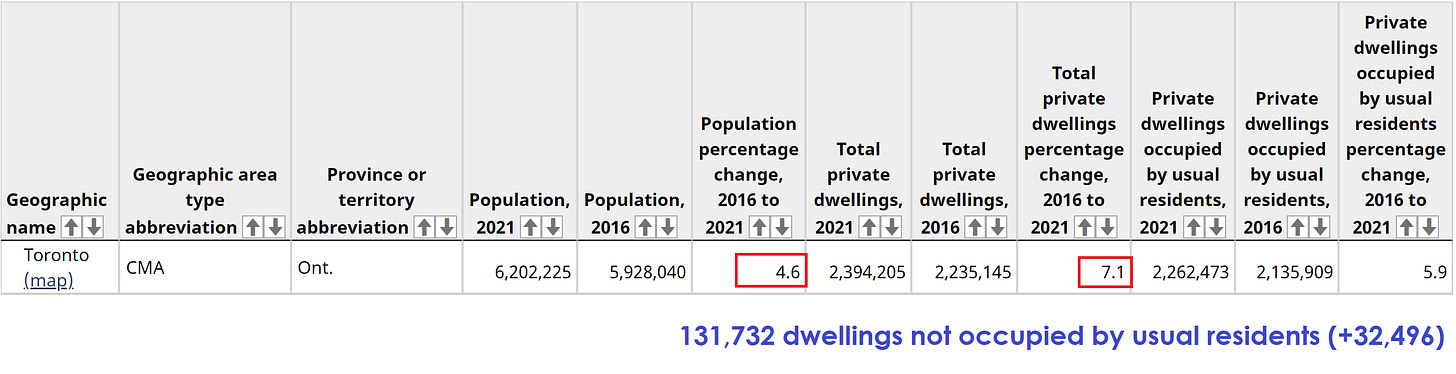

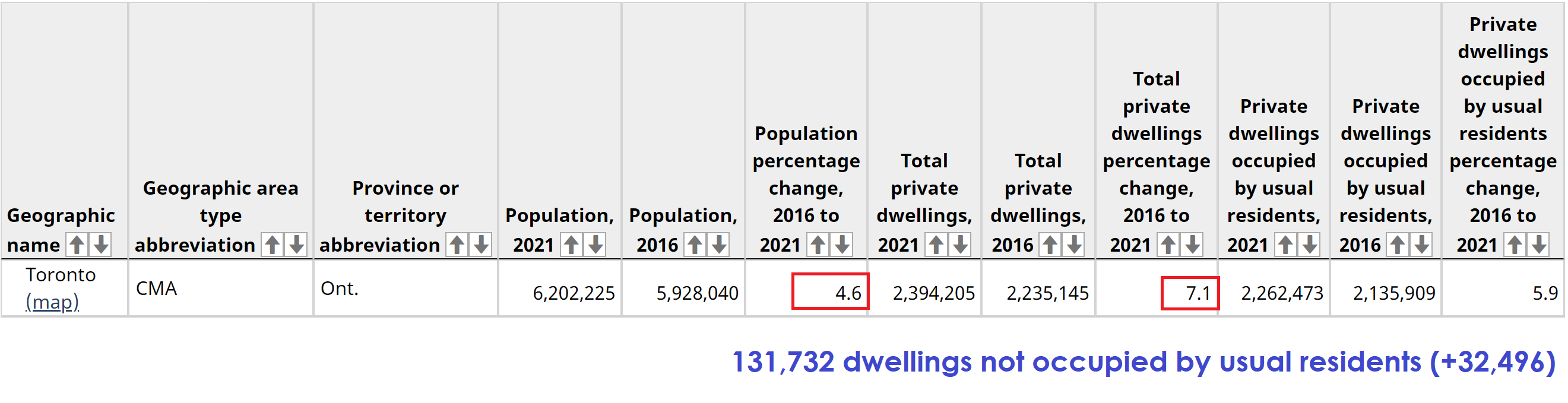

Toronto CMA population increased by +4.6% and housing stock by +7.1% during the last 5 years.

Increase of 32,496 dwellings not occupied by usual residents compared to 2016.

I’d like to elaborate here because this topic is very important and controversial at the same time. I’ll start with the justification for why I’m comparing the population growth rate to the rate of housing stock change. Someone said to me that it’s a “sloppy way” and I completely agree with it. 100,000 completed 1 bedroom units and 100,000 completed 2br units can house different amounts of people but both are 100,000 units on paper.

However, in order to make a proper comparison, accurate adjustments need to be made for both supply and demand side, additional factors should be accounted for such as household size change due to the aging population etc. Those adjustments are very complex and require data which I don’t have so I can’t produce those myself. Also so far I haven’t seen any analysis which accounted for all the factors accurately enough so instead of making incomplete adjustments leading to wrong conclusions I’m working with raw, but accurate data, even if it’s sloppy. It doesn’t give an exact answer but it gives a clue.

Here is an example of why comparison of just the rates of change is appropriate. Three scenarios are presented:

Housing stock and population both grew by 10%

Housing stock grew by 5% and population by 10%

Housing stock grew by 10% and population by 5%

Even though the base numbers for housing stock and population are different you can directly compare rates of change to get a clue about a potential shift in the supply/demand balance. Again this is a sloppy approach but it’s not an incorrect one.

Are we having housing shortages in the GTA? Absolutely. Does that mean we are not building enough? Not necessarily, this is an extremely difficult question to answer.

The key factor here in my view is: Are the causes of housing shortages sustainable and permanent? If they are, then we are clearly not building enough but what if those shortages are driven by temporary factors like demand from non-permanent residents or units intentionally kept vacant by speculators?

Do we know how sustainable is this source of housing demand is and if it’s going to decline in the future or not?

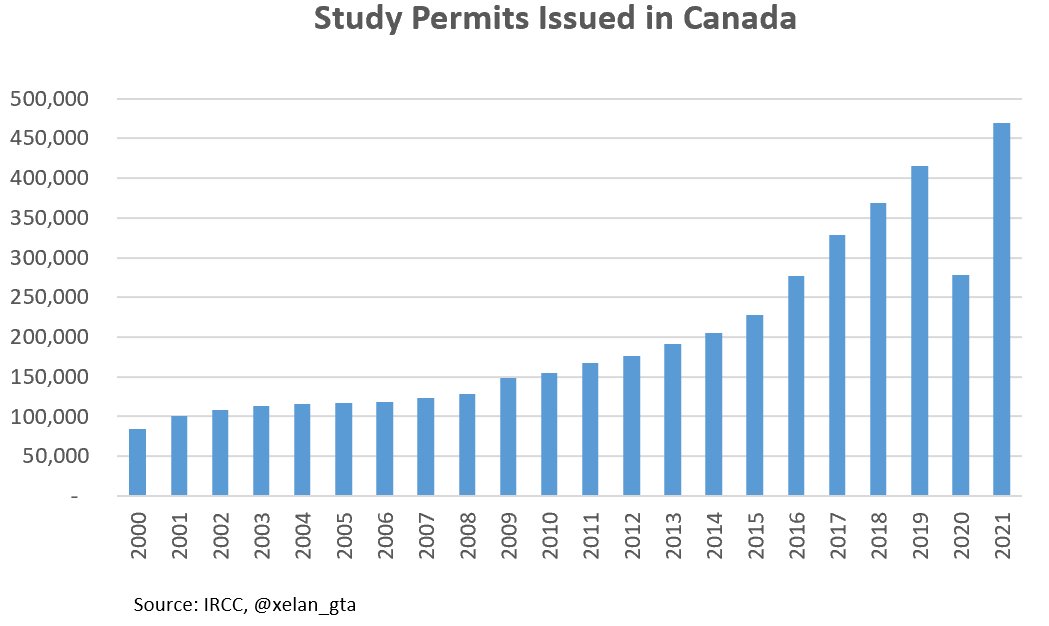

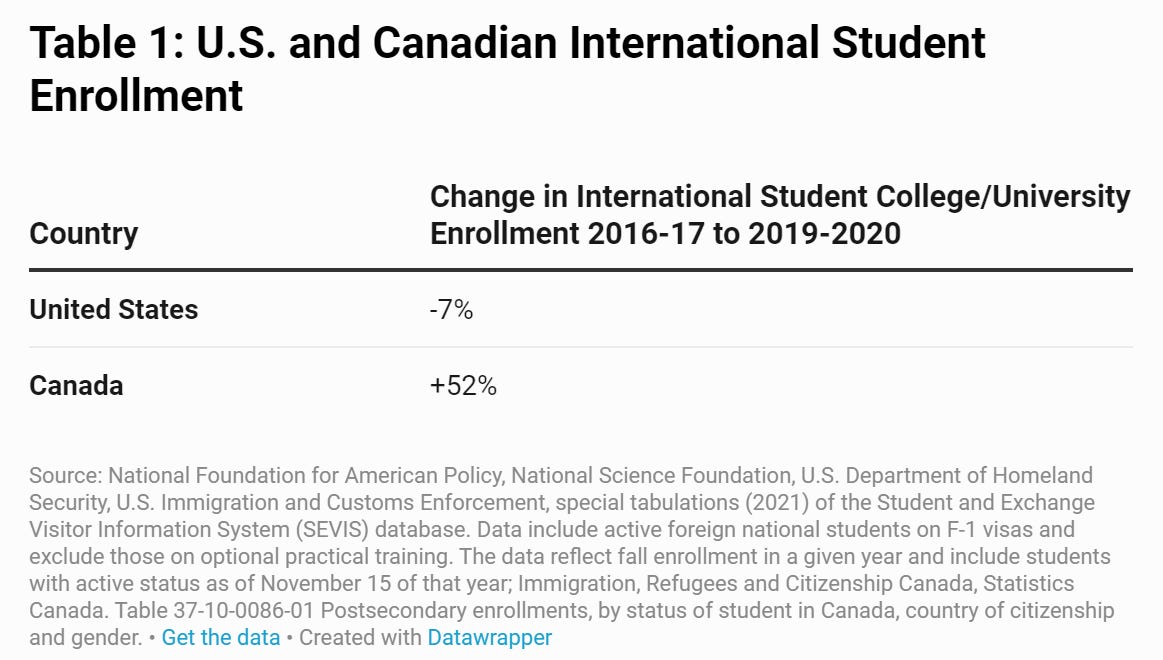

Especially since Canada has been effectively “stealing” enrollments from the US in recent years.

I simply don’t know, that’s why I can’t tell with absolute certainty if we are building enough or not. If the number of study permits permanently declines it will unlock a significant amount of housing supply. This could come naturally or artificially, for example, due to a shift to easier immigration paths for international students in the US or ruling party change in Canada which will set a cap on study permits in an attempt to address housing shortages.

Also, housing bubbles are often followed by overbuilding, so I’m spending a great amount of time trying to figure out which factors are preventing the detection of overbuilding during the formation of the bubbles.

Conclusions

Toronto Metro real estate market continues to be exceptionally strong however there are signs it could be starting to run out of steam. In February a significant increase in the new listings occurred which resulted in the accumulation of the active inventory well in excess of seasonality. Strong sales masked it to some extent but both market balance indicators weakened.

It is important to note that we are not talking about price declines or even about stabilization at this point, we are talking about market becoming less crazy. Prices are still expected to continue growing in the short term. However, every market shift starts somewhere and I believe it’s more likely that it already happened. Future data will bring more clarity.

The main reason of the new listings acceleration in my view is related to anticipation of higher interest rates in the future which will lead to the market cooling.

Today prices are growing at a time when mortgage rates are also rising which leads to exceptionally fast deterioration of the housing affordability and investment attractiveness metrics such as cash flows. Both of those metrics already worsened to unprecedented levels.

In January 2022 Toronto overcame Vancouver as the most expensive metro market in Canada. It retained the leadership in February and the price gap increased a little. Toronto is experiencing rapid growth in luxury ($2M+) property sales with the condo sector being stronger than the single-family one.

Rental market is quite strong in the condo segment and quite weak in the purpose-built rental segment. Market balance and seasonality for condo rentals is pointing to the upside risk, but rent prices are already elevated which limits upside potential before further growth meets market resistance.

Sales in the new construction segment were very strong in February thanks to the condo segment. That will lead to more housing supply down the road.

The government released a new immigration projection with increased targets for 2022-2023 compared to the previous one. This year's target was increased by 20,635 mainly due to refugees and humanitarian categories.

Census data revealed several interesting trends showing that the rate of population growth in Toronto Metro is declining and also that housing stock is growing faster than population. It likely means that housing shortages are becoming smaller but it needs to be analyzed more in detail to get to the right conclusion. The question of whether we are building enough or not is extremely complicated due to a number of unknown variables and projections. There was also a material increase in the number of units not occupied by usual residents. This is a notable development, however, Census data was collected during the onset of the pandemic so it could be distorted. Also, this metric can be misinterpreted so check this post to get more clarity.

Heartbreaking war in Ukrane brought a lot of economic uncertainties and created additional risks and inflationary pressures. In the coming month I’ll be laser focused on the Toronto Metro active listings, sales, macro developments, commodity prices and the upcoming interest rate decision by the Fed.