Canada's Population Growth is Still Strong but Likely Approaching a Turning Point

[PAID CONTENT SAMPLE] Overview of important developments in the Toronto Metro housing market and macro reported in November 2023

Highlights

Toronto Metro is a buyer’s market but inventory and market balance stabilized.

The rental market remains balanced.

New construction unsold inventory is growing.

Housing affordability is improving.

Record inputs into population growth continue, but the pace is slowing down.

Seven risks to international student admissions in 2024.

Soft landing is progressing for the Canadian economy with growth in unemployment, mortgage arrears, delinquencies and credit card debt.

Resale and Rental Markets

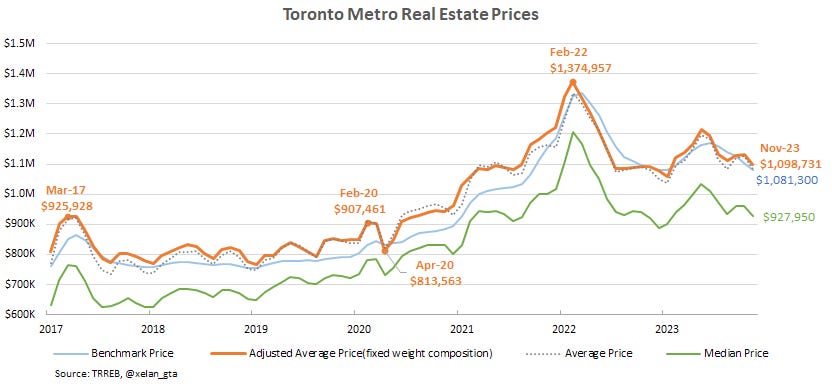

In November, the Toronto Metro Real Estate Market showed some signs of stabilization. New listings experienced a slight decline, while sales increased compared to the 10-year average. Moreover, there was a notable rise in terminated listings, at a scale last observed in 2009, contributing to the active inventory resilience.

Market balance indicators also stabilized, albeit at historically weak levels.

Recently price metrics acted differently, but I recommended focusing on the overall downtrend rather than monthly fluctuations (link) (link2). In November, all price metrics finally aligned and displayed declines. Seasonality is a contributing factor here but it’s not the main story.

Prices were relatively unchanged from the previous year and 19-23% below the 2022 peak values. Further declines are expected in the short term.

The rental market also demonstrated some stabilization in November. The market balance weakened, however, after adjusting for seasonality it stayed unchanged compared to the previous month. The rental market is balanced so rents should remain stable.

As expected, rent prices decreased in November, primarily attributed to seasonality (link).

The annual rent price growth in November was 4%, which is a significant slowdown from the 18% observed in June 2022.

New construction sales remain weak, mirroring the dynamics of the resale market. A noteworthy development in October(the latest available data) was a further increase in unsold inventory, surpassing the peak observed in 2019.

Housing Affordability

The minimum discounted mortgage rate declined by 0.2% in November for the first time since April 2023.

Combined with the decline in real estate prices it resulted in housing affordability to improve from 68% to 65%. It now requires 65% of typical household income to service mortgage payments on the newly purchased typical property in Toronto Metro.

This is the second consecutive affordability improvement in 2023 and it is expected to continue.

Population Growth

September saw robust data for aggregate non-permanent resident permits, surpassing previous years' figures.

Combined all population growth inputs in Q3 2023 were record high so a new population growth record should be expected in the upcoming data unless there were also strong outflows which I’m unable to track.

However, upon closer inspection, September witnessed the smallest increase in non-permanent resident permits in 2023 compared to the previous year.

In the previous newsletter, I stated (link):

The latest data indicates that inputs into population growth are not slowing down yet, but they definitely will slow down eventually warranting close attention to the data.

It didn't take long for the first signs to emerge. The inclusion of immigration data is causing annual growth to further decrease from 28% to 15%. This is a consequence of Canada’s intensifying immigration efforts in the first half of the year, necessitating a slowdown to land on the targeted 465,000 for 2023.

Global demand for international education is expected to grow in 2024, however, Canada faces some challenges:

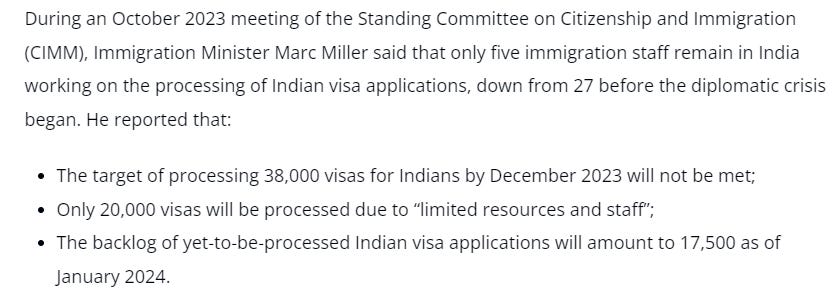

The strained relationship between Canada and India, resulting in the expulsion of 41 Canadian diplomats(link), is now impacting visa processing.

Sentiment in India towards Canada may be shifting, as indicated by Vinay Chaudhry, CEO of Worldwide Educonnect:

"Two years ago, if somebody would get an offer letter from a Canadian institution, the parents and friends would say 'wow!' but now they say 'why?' – i.e., 'why are you thinking of Canada now?'"

While Canada has reduced visa processing capacity in India, the US is expanding it(link) (link2).

Canada introduced a new verification process for letters of acceptance to combat fraud (link).

“Starting December 1, 2023, post-secondary designated learning institutions (DLI) will be required to confirm every applicant’s letter of acceptance directly with IRCC.”

A temporary measure allowing international students to work more than 20 hours per week is set to expire on Dec 31, 2023 (link). There is a s strong push to have this policy extended or made permanent, however, I will be surprised if it happens.

Similarly to Canadians, international students are struggling with rising prices and housing affordability (link).

Competition for Permanent Residence has intensified in 2023 due to record international student admissions, post-graduate permit extensions, the influx of 200,000+ Ukrainians under the Canada-Ukraine Authorization for Emergency Travel (CUAET) program, new Tech Talent Strategy (link), immigration stream for Ukrainians (link), healthcare workers(link), individuals from Hong Kong(link) and others.

India is in the spotlight because the most international education demand in Canada comes from there. It’s important to note that similar tightening related to international student admissions is occurring in other countries, notably Australia and the UK. The uncertain landscape and numerous risks make it challenging to predict the resulting demand for Canadian education in 2024. Valuable insights on this topic are expected in January-February 2024 when study permit data for winter admissions is released.

Coupled with the phasing out of the CUAET program discussed in the previous newsletter(link), it's increasingly likely that the records of new non-permanent resident permits and population growth seen this year won't be surpassed in 2024 and will start declining. The magnitude of the potential decline can be quite large and warrants a separate article.

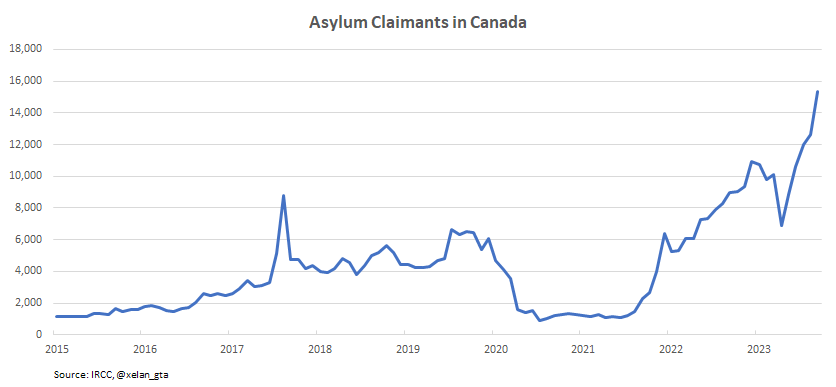

Lastly, on the topic of population growth, there's notable growth in asylum seekers.

This is important to monitor, especially considering the annual immigration quota allocated for refugees in 2024 is 76,115, translating to 6,343 average monthly admissions.

Macro

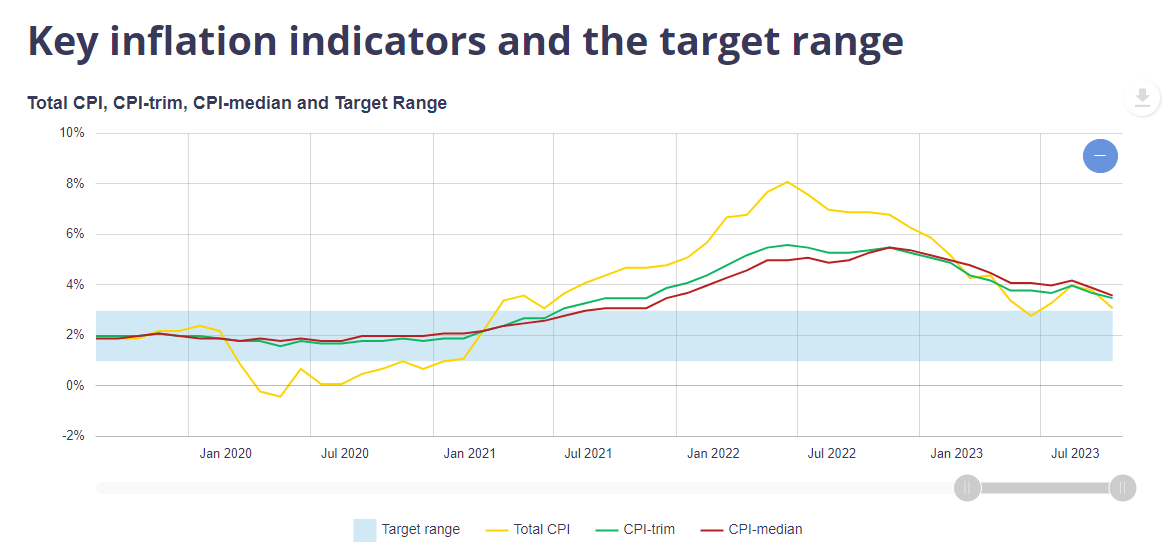

So far, the soft landing scenario engineered by the Bank of Canada is working.

Inflation is on a downward trend, and there is a gradual increase in the unemployment rate and mortgage arrears.

As well as insolvencies and credit card debt.

While the current levels of these indicators are not cause for immediate concern, they are interconnected with the growing financial stress faced by property owners.

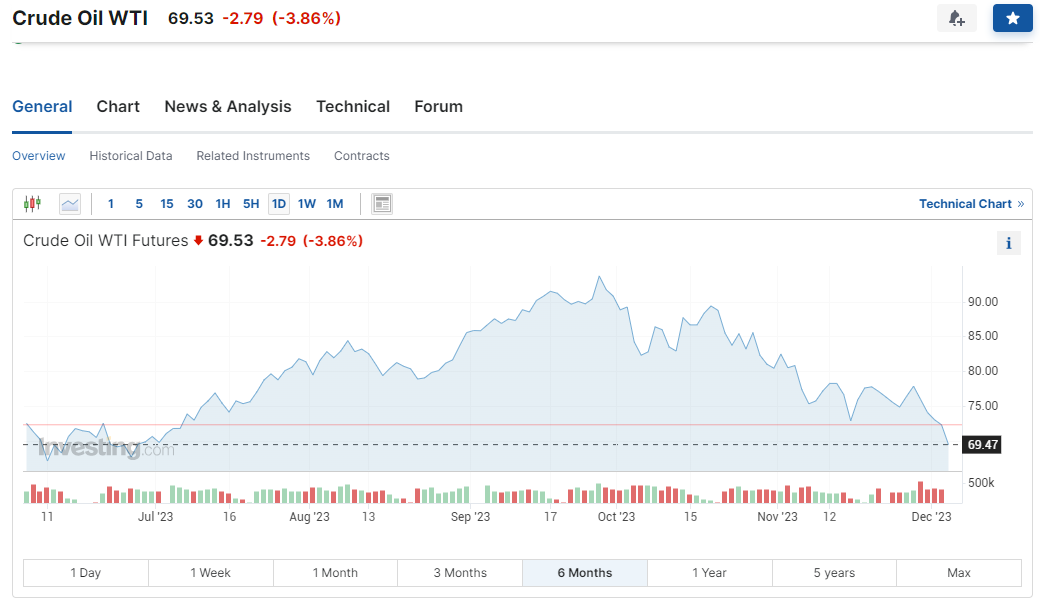

In the July 2023 newsletter, I flagged elevated oil prices as a potential risk for higher inflation(link). I must note that, due to recent declines in oil prices, this specific risk has temporarily subsided. However, this may change in the future.

Conclusions

The Toronto Metro real estate market exhibited some stability in November. Sales saw a slight increase, and new listings declined compared to the 10-year average. Notably, there was a surge in listing terminations, the highest since 2009 on a seasonally adjusted basis.

Sellers are actively trying to stabilize the market by removing listings, but this may be challenging due to higher rates and a growing number of distressed sellers. So far, there has been limited success, resulting in a stabilization of active inventory, which stopped growing and remained largely unchanged on a seasonally adjusted basis. Market balance indicators stabilized as well, but remain in a buyer's state. As a result, all price metrics declined in November which is expected to continue. Overall, prices were relatively unchanged from last year and 19-23% below the 2022 peak values.

New construction sales followed a pattern similar to resale, however, there was a notable increase in unsold inventory surpassing the 2019 peak. The Toronto Metro rental market stabilized in November around the balanced zone, with rent prices expected to closely follow the seasonal patterns in the near term. A 0.2% decline in minimum 5-year mortgage rates coupled with lower prices resulted in an improvement in housing affordability. Toronto Metro real estate market remains historically very unaffordable but further improvements are expected.

It's essential to note that the stabilization in both resale and rental markets was only observed for one month, making it impossible to draw conclusions about pivotal moments based on such limited data. Future data should bring more clarity.

Inputs into population growth remain at record highs, however, there is notable deceleration. Despite anticipated global demand growth for international education, Canada faces challenges such as a strained relationship with India, reduced visa processing capacity, potential shifts in sentiment, increased competition from the US, new measures like study permit verification and reinstatement of the 20-hour per week work limit, affordability issues, and increased competition for permanent residence. With the CUAET program winding down, it's more likely that both new permits and population growth will decline in 2024, though the extent cannot be estimated at this point.

On the macro front, a soft landing is gradually progressing. Indicators such as unemployment, mortgage arrears, delinquencies, and credit card debt are slowly increasing. The big picture may obscure individual cases of those on the financial edge, masking potential risks, but little data is available on such cases. Inflation is gradually returning to the target, and a recent decline in oil prices may expedite this process.