Real Estate Market is Ice-Cold Despite the Population Growth Tsunami

Overview of important developments in the Toronto Metro housing market and macro reported in September 2023

Highlights

Toronto Metro real estate market is exceptionally weak.

The rental market reached a balanced state and rents started to roll over.

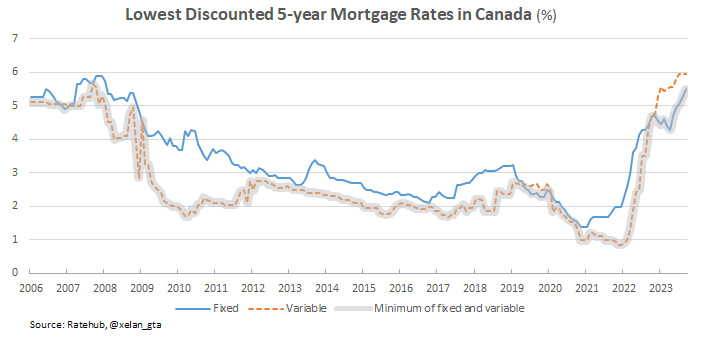

Minimum 5-year mortgage rates continued to rise.

A spike in Toronto Metro housing completions in August.

Population growth is record-high with strong leading indicators.

Inflation is overshooting the Bank of Canada projection.

Resale and Rental Markets

The Toronto Metro real estate market experienced a significant weakening in September. There was an increase in new listings compared to the 10-year average, while sales declined, leading to a notable rise in the number of active listings. All these trends are visually represented in the following chart.

For the month of September, sales reached their lowest point since at least 2006, and all these factors contributed to a deterioration in the market balance indicators. One of these indicators, "Months of Inventory," hasn't been this weak since 2009.

Another market balance indicator, "Sales-to-New Listings," is even weaker, hitting its lowest point for the month of September since at least 2006, surpassing even the levels seen during the 2008 downturn.

It is a firm Buyer’s Market, and if these conditions persist, significant price declines may be experienced by year-end. However, meanwhile, some price metrics increased in September due to factors like seasonality and a higher proportion of single-family and luxury properties being sold.

The seasonally adjusted average price reported by TRREB decreased by 0.1% monthly in September. As shown in the chart, the data exhibits some noise, so it's advisable not to place too much emphasis on monthly fluctuations. Nevertheless, the market remains exceptionally weak, and prices are expected to continue declining unless there is a change in the current conditions.

In general, prices are 1-4% higher compared to the previous year but remain 16-20% lower compared to the peak in 2022.

The rental market has also been gradually weakening and has now reached a balanced state.

Rent prices have started their seasonal descent, with both condo and house rents coming down from their previous highs.

Mortgage Rates

In August, the discounted 5-year fixed mortgage rates continued their upward trend, resulting in an increase in the minimum 5-year mortgage rates.

Although variable mortgage rates remained stable, they are irrelevant to housing affordability due to the low share of new variable mortgages in recent times.

The rising mortgage rates are counteracting price declines and are keeping housing affordability and the attractiveness of real estate investments at record-worst levels.

Housing Construction

August saw a significant surge in housing completions in the Toronto Metro area, with 8,718 units completed. This figure is more than three times higher than the historical average.

While this development is positive news and likely contributing to the weakening of the Toronto Metro rental market, it still falls short of meeting the demands generated by rapid population growth.

In August, new construction sales experienced a further decline, bringing the year-to-date number to the lowest level in at least the past seven years.

In September, the Federal Government introduced an enhanced GST rebate for rental construction (link), aimed at incentivizing the construction of purpose-built rental properties. This move is expected to partially offset the decline in new condo construction caused by the low pre-construction sales. In some cases, planned condo projects may even be converted into purpose-built rentals.

However, it's important to note that rental starts currently account for only about 22% of all apartment starts, so the full impact of this measure on the housing market remains to be seen.

Population Growth

The tsunami of population growth in Canada continues. The most recent official data, covering the second quarter of 2023, revealed a new record for population growth, reaching 1,158,705 individuals. Those who closely follow the data may recall seeing a previous figure of 1,200,000. That number was revised down to 1,094,713.

Non-permanent residents continue to be the primary driving force behind this trend, with an unprecedented increase of 233,361 individuals in the second quarter of 2023.

It is reasonable to assume that the current rate of population growth is unsustainable. However, even leading indicators do not yet suggest a slowdown. For instance, the number of issued permits for non-permanent residents and new applications for such permits continue to set new records.

In July alone, there were 91,299 new applications and extensions for temporary residency submitted by Ukrainians.

It will take some time for these applications to be processed before any of them are reflected in the official population growth data.

Another example is the Labor Force Survey (LFS) data, which provides the latest estimate for the working-age population in August 2023, once again reaching a new record high.

Given this explosive population growth, it is crucial to note that all the official data is lagging (August) and in some cases significantly lagging (June-July). Therefore, there is no question about where all those people are going to live because they already found housing by now.

Inflation

Inflation in Canada regained momentum in August with all metrics posting an increase. This development represents an upward deviation from the inflation projection provided by the Bank of Canada in the July Monetary Policy Report (MPR) and may require higher interest rates if persists.

Conclusions

Following some signs of stabilization in August, the Toronto Metro real estate market resumed its downward trend in September, primarily driven by the condominium sector. New listings and active inventory increased compared to the 10-year average and sales declined to a record low level for the month of September.

Consequently, market balance indicators weakened to levels not seen since 2009. However, despite this market weakness, average and median prices experienced an increase in September. This uptick can be attributed to seasonal factors, a higher percentage of single-family and luxury property sales. It didn’t come as a surprise, in my previous newsletter, I cautioned about a potential seasonal uptick in September (link). Presently, price metrics do not provide reliable signals due to the exceptionally weak market balance, leaving no doubt that it's a buyer's market. Consequently, it is fully expected that underlying prices will decline in the near term unless there is a change in the current conditions.

The Toronto Metro rental market continued its gradual decline, reaching a balanced state in September. Rent prices are coming off their peak and are anticipated to gradually decline further toward the end of the year if conditions persist.

Minimum 5-year mortgage rates continued their upward trajectory in September, maintaining housing affordability and the attractiveness of real estate investments at record-worst levels.

In terms of housing construction, the most notable development was a surge in housing completions in August, with nearly 9,000 units completed, more than three times the usual level. New construction sales remain low, which is expected to result in a decrease in housing starts. However, the enhanced GST rebate is poised to provide a partial boost to rental construction, offsetting some of the decline.

Population growth in Canada continues to set new records, with the latest quarter witnessing the highest-ever number of net non-permanent residents. Over the past four quarters, the Canadian population increased by nearly 1,160,000 individuals, and leading indicators suggest that this robust population growth will persist for some time. However, housing and infrastructure are ill-prepared for such rapid population growth, leading to public frustration. The government is starting to listen and consider introducing caps(link) and even adjusting immigration targets(link), which was unheard of six months ago. It is inevitable, in my view, that the population growth rate will decrease; the only question is when.

Inflation in Canada reaccelerated in August, with all inflation metrics trending upward. This represents a departure from the inflation projection shared by the Bank of Canada in July and may require higher interest rates if the trend persists.

Note: I plan to publish the second part of my article “The current state and what's next for the Toronto Metro housing market?”(link). It will retrospectively analyze previous conclusions, provide an overview of the current state, and offer insights into future expectations. This article will not be sent by email so those who are interested, please wait for an announcement on Twitter later this month.