Rental Market is Tight and Unaffordable but Relief Could be on Its Way

Overview of important developments in the Toronto Metro housing market and macro reported in January 2023

Toronto metro real estate market continued to stabilize in January. Prices declined by about 22% from the peak and are expected to remain stable in the near term. Historically the market balance indicators we are seeing today correspond to stable prices.

Real estate industry professionals are reporting an uptick in activity.

Data from January doesn't reflect that uptick yet but it doesn’t mean anecdotes are incorrect, it requires time for activity to translate into firm sales and be reflected in the stats. Most likely we’ll see it in February’s report and obviously, I mean an uptick above the seasonal expectations.

Conceptually it makes sense, the market has been weak for so long, sales are way below normal levels and fixed mortgage rates are starting to come down. Markets rarely change in a straight line so it would be strange if we didn’t have at least a slight uptick at this point. It doesn’t mean we are looking at a mid/long-term market bottom though. Valuation metrics continue to be pretty bad both for investors and homebuyers. Here is the chart showing exactly where we are now in terms of housing affordability.

Price correction and fixed mortgage rates decline improved affordability a little but Toronto Metro real estate market continues to be the most unaffordable in decades.

Macro

Financial stress caused by the rising rates and cost of living may lead to an uptick in new listings. I’m closely watching the indicators but so far I see no immediate concern in the data.

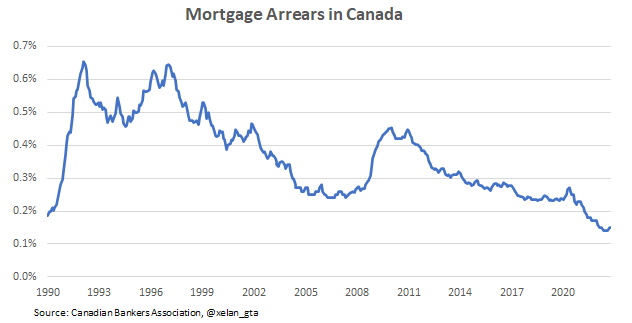

The latest mortgage arrears data shows a slight uptick but it’s within the range of data fluctuations.

It’s very possible we are witnessing a turning point here but in any case, the current level is among the lowest since at least 1990.

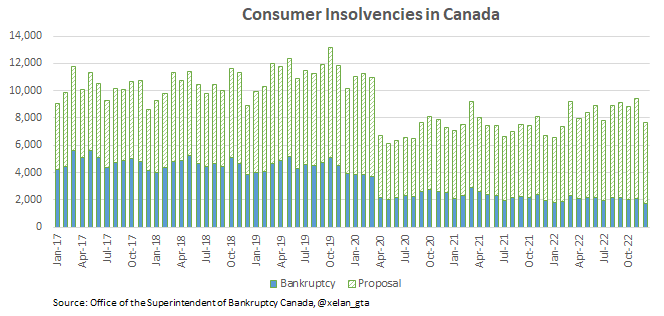

Insolvencies are picking up too, but again, still very low historically, especially the share of bankruptcies.

Rental Market

Toronto Metro rental market remains tight but stable. We are entering a strong season now so rent prices are expected to resume growth. It is already the most unaffordable rental market in at least the last 30 years and in the short-term likely become even worse before it gets better.

Population Growth

One of the important pieces of data released in January was the annual Toronto Metro population growth.

It reinforces an important trend of growing population outflow from Toronto Metro to other cities within Ontario(intraprovincial) and to other provinces(interprovincial) as well. An increase in outflows is believed to be linked to housing affordability so while Toronto Metro remains unaffordable compared to other places in Canada elevated outflows are expected to continue. This trend is so significant in my view that I included it in my 10 Best Charts of 2022 (link. ← Other great charts here too)

2023 Housing Completions

Another interesting piece of data released in January was insight from analytical firm Urbanation forecasting nearly 32,000 GTA condo completions in 2023. (link) This is big news since the previous record was 22,473. In addition to 32,000 condos 7,740 purpose-built rental units are expected to be completed in 2023 as well. This gives a total of nearly 40,000 apartment units for 2023.

Later on, Urbanation clarified that “the figure may more realistically be in the ballpark of 25,000 to 30,000 units — he says the industry typically falls short of its projected deliveries” (link)

To give you a perspective here is how this forecast stacks against historical data.

Unfortunately, I don’t have historical completions data from Urbanation so I’m using the one from CHMC which is different due to methodology. That’s why I had to average data for 2013-2015 years to keep it more in line with Urbanation’s reporting.

I have a model allowing me to roughly forecast completions and this model also points to 35,000 units as a median scenario for apartment completions. So, again, my estimate is very rough but it’s in the same ballpark.

I’d like to elaborate on the part: “industry typically falls short of its projected deliveries” mentioned by Urbanation. Indeed, it was the case in the past but due to the low number of new projects expected to be launched in 2023 constraints experienced by the construction industry may start to ease, leading to the faster completion of existing projects. I won’t be surprised if in 2023 construction industry won’t fall short and will outperform instead.

Inflation Projection

Bank of Canada increased the policy rate by another +0.25% in January to 4.5%. They also released Monetary Policy Report revealing the second consecutive downward revision to inflation projection. The good news, inflation is coming down faster than expected so far.

During the press conference, the Bank of Canada communicated that they will be pausing with the rate hikes for now while observing the impact of the previous tightening. They said it’s too early to even think about rate cuts right now but further rate hikes are possible if inflation is not going to come down as fast as they expect. Bank of Canada’s projection indicates that we should see inflation coming down to 3% by the second half of this year.

We can see how widely inaccurate projections were in the past but the most important message here - if inflation fails to come down as fast as indicated here additional rate hikes should be expected.

Conclusions

Toronto Metro prices continue to decline but the pace is slowing down and market balance indicators reached a balanced state when typically prices are not changing much. Real Estate industry professionals are reporting an uptick in interest from buyers so we could see this uptick reflected in February data.

Regardless if we are going to see an uptick or not in my view it’s very early to make conclusions about medium/long-term market bottom. Housing Affordability and Investment Attractiveness are still among the worst in history and even if the Bank of Canada cut interest rates by 1% it’s not going to improve those metrics significantly enough. At this moment the Bank of Canada is communicating that discussion about rate cuts is very premature.

There is an uptick both in mortgage arrears and insolvencies but they remain near historical lows so no immediate concern about those developments but important to continue monitoring.

Toronto Metro rental market remains tight and is entering a period of strong seasonality when rent prices typically grow. Data for rental apartments released by CMHC is indicating that rental affordability is the worst in at least the last 30 years so there will be strong resistance to further rent increases.

One of the resistance methods is relocation away from Toronto Metro. Population growth data is clearly showing that this trend is picking up steam and more and more people are leaving Toronto Metro every year.

Another relief for Toronto Metro rent prices in 2023 may come from the housing supply. A new record, nearly 40k of combined condo and rental apartment units could be completed in 2023 according to analytical firm Urbanation. This is almost double the 10-year average. Completions modeling that I performed confirmed that insight. Also due to the slowdown in new project launches, I believe the construction industry could surprise the market with sooner unit deliveries.

Those new construction stats don’t matter much if Canada’s population grows by 1,000,000 per year however if the population growth slows down in 2023 high number of newly constructed units coupled with population outflow from Toronto Metro may start making a positive impact on the rental market balance. In my view, that’s a more likely scenario than another 15% growth in rent prices.