Turning Point For Real Estate Market is Confirmed

Overview of important developments in the Toronto Metro housing market and macro reported in February 2023

Before we start, a little announcement for institutional investors, builders, lenders, and other organizations that heavily rely on real estate analytics to conduct their business. Please enquire about the new research, created exclusively for you. Details in the post:

Resale Market

In a previous newsletter, I shared anecdotes from real estate industry professionals about a notable increase in homebuying activity in Toronto(link). However, the monthly statistics did not support it at the time. As expected, this activity finally showed up in February's data in a very convincing way.

The market has undoubtedly started tightening based on almost any metric you choose. This conclusion remains true even after adjusting for seasonality.

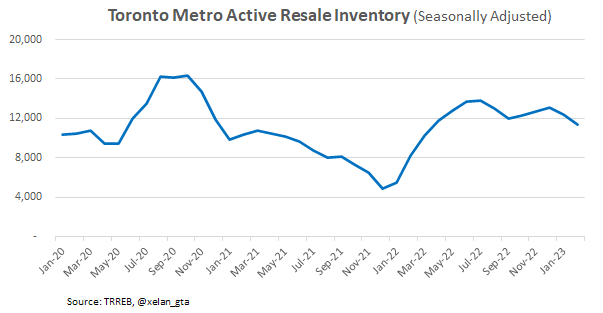

Toronto Metro active resale inventory, which I’m tracking weekly, is declining on a seasonally adjusted basis.

I would like to clarify that I don’t know what kind of rebound we are facing. Will it be a small uptick followed by a further market slowdown, or a medium/long-term market bottom? Setting aside speculation about the future, it is important to acknowledge that the market is turning, and if your view is bullish, this could be an opportunity. While I regularly express my views on this topic (Jan 2023 newsletter), I was wrong in the past so keep that in mind.

Rebound appears to be consistent across housing segments in the Toronto Metro area. The detached sector is currently leading the rebound in terms of prices, but this is not reflected in the market balance and could be attributed to seasonality, composition mix, or other factors.

All four tracked price metrics increased in February compared to January.

There are several reasons for the market tightening, and it's important to highlight that it's not solely due to strong sales. While sales increased compared to January, this growth is modest after adjusting for seasonality, and the level of sales is still historically low.

In my view, the continued low number of new listings is the bigger story compared to the uptick in sales.

This is because I find it difficult to envision a significant rebound in sales until a decline in mortgage rates is certain.

Rental Market

The rental market remains tight, with market balance indicators similar to those seen between 2017 and 2019. Therefore, this period should serve as a reference for the current rental market. Rents are expected to rise in the short term due to market tightness and seasonality. However, it's also possible that rental unaffordability could start limiting further increases.

An increase in the number of completed housing units is anticipated in 2023, which could potentially provide some relief to the rental market. However, in January, the number of completions was consistent with the historical average.

New Construction Sales

New construction sales were very low in January, according to the latest available official data.

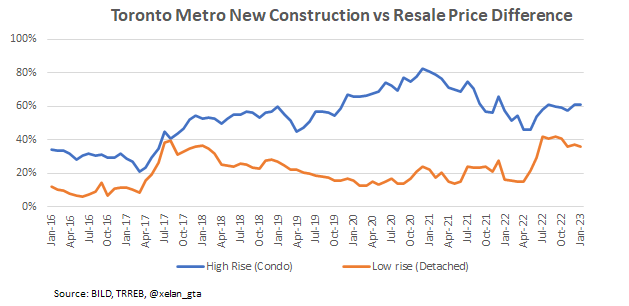

Anecdotally, several agents reported an uptick in new construction sales in February, which makes sense. However, despite the pickup in resale activity, the new construction sector remains at risk due to high price premiums.

In order to restore historical price premiums, either new construction prices need to come down or resale prices need to increase.

Macro

At the moment, financial indicators for households look okay. In fact, savings rates even increased in Q4 2022.

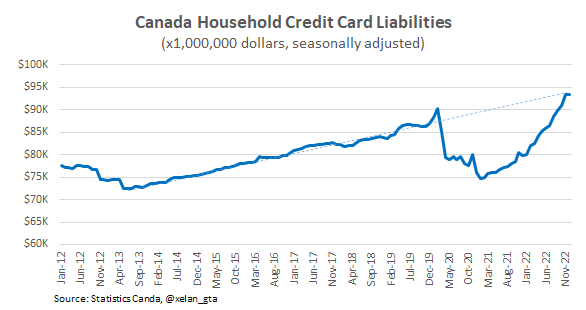

While credit card debt is growing rapidly, it has only recently caught up with the pre-pandemic trend.

Therefore, while the rate of change is alarming, the level isn't yet a cause for immediate concern.

The money supply, which can be seen as a "fuel" for asset prices, deserves attention. Growth rates for two money supply aggregates went negative for the first time since at least 1996.

Definitions of those “M”’s can be found here. While this decline looks impressive, it is partially a result of the base effect (a comparison to the previous year's spike). Overall, the money supply is in line with the trend observed since 2012, however, growth almost stalled in 2022.

Since 1969, money supply M2++ has been growing at an average annual rate of 9.2%. During the past year, it increased by only 2.8%, which indicates a significant slowdown that deserves attention. While monetary policy remains tight it’s reasonable to expect money supply growth to remain below the historical average.

Non-Permanent Residents

The number of non-permanent residents in Canada has increased from 300,000 to nearly 2,000,000 over the past 20 years, with the majority of this growth occurring in the last 6 years.

A significant uptick was observed in 2022 which was a result of an increase from all 3 major non-permanent resident categories. An important contributing factor was a new measure allowing Ukrainians affected by the war to temporarily come to Canada. The impact of this program is significant, with over 900,000 applications received and nearly 600,000 approved. Out of those 600,000, only about 170,000 have arrived in Canada so far, which is about 30% (link). It remains unclear whether the remaining applicants will come to Canada, but the potential for further population growth boost is present. Also, statistics are lacking details about the number of applications which were submitted but haven’t been processed yet.

Conclusions

The real estate market in Toronto demonstrated a strong rebound across all housing types in February, with rising prices supported by a tightening in market balance indicators. It could represent a potential opportunity for those who hold a bullish view. Personally, I am skeptical about the sustainability of this rebound, but I am not ruling out any possibilities. Market tightening was a result of an uptick in sales but also a low number of new listings which remains a main story in my view. New construction sales continue to be slow, and prices remain high compared to the resale market.

The rental market in Toronto remains tight, with rents expected to rise in the short term due to the combination of market tightness and seasonality. Although a high number of housing units is anticipated to be completed in the Toronto Metro area in 2023, data for January completions does not support this.

Low number of new listings is understandable since financial indicators for households look okay, with savings rates increasing in Q4 2022. Credit card debt is growing rapidly, which warrants attention, however, the overall level is not concerning at the moment. Another important development is a significant slowdown in money supply growth. It is expected to remain below the historical average as monetary policy remains tight, limiting asset values growth.

The number of non-permanent residents in Canada has risen sharply over the past 20 years, with a significant increase in 2022 due in part to a new measure that allows Ukrainians affected by the war to temporarily stay in Canada. While only about 30% of approved applicants have arrived so far, it is uncertain if the rest will follow. Their potential arrival could further boost Canada’s population growth.