Real Estate Market is Turning South

Overview of important developments in the Toronto Metro housing market and macro reported in June 2023

Highlights

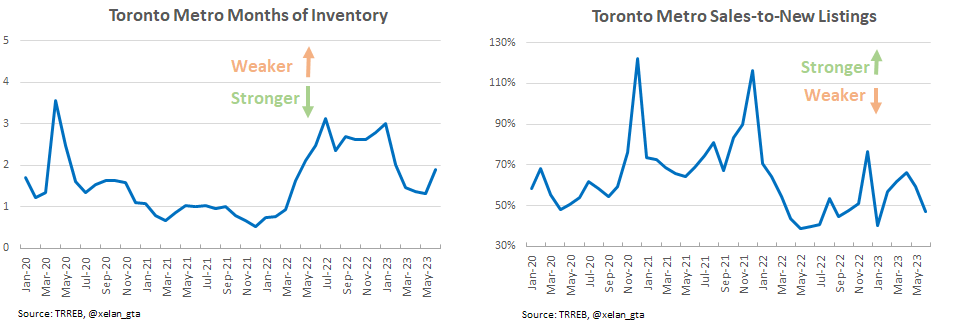

Toronto Metro resale market is weakening

Toronto Metro rental market is strong and stable

Why the market is weakening?

New record population growth

Interest rate increases are working

Resale and Rental Markets

In my previous newsletter, I drew attention to a notable increase in Toronto Metro new listings and suggested that:

“It could potentially be a turning point in the market dynamics.” (link)

June’s data reinforced that view, as new listings continued to rise unusually for this time of the year, while sales started to decline.

These developments led to a sharp increase in active inventory and weakened both market balance indicators.

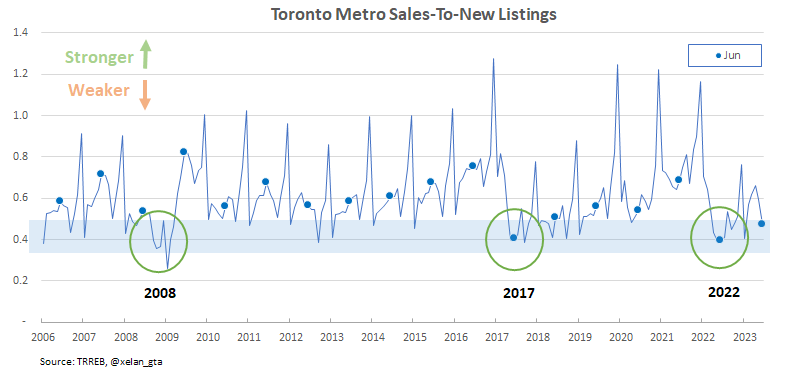

It's noteworthy that the Sales-to-New Listings ratio declined to levels comparable to those observed during housing corrections in 2008, 2017, and 2022.

This indicates that the market shift is not a minor adjustment but a compelling change witnessed in both the single-family and condo segments.

Prices generally continued to rise in June, since transitioning the market from a seller's to a balanced or buyer's state takes time.

Different price metrics behave differently, and they all have flaws, making it challenging to precisely gauge price changes during periods of rapid market shifts. Here is the monthly change for all key Toronto Metro price metrics.

If the current market dynamics persist in July, it's highly likely that the Toronto Metro prices are around their peak levels.

The rental market remains tight but stable, with rents continuing to grow.

Despite Toronto Metro experiencing record-high population growth, the rental market has held up exceptionally well. In fact, the average rent price increase aligns with the typical seasonal pattern observed over the last decade.

While it may appear confusing, there is a logical explanation for this behaviour. If your business relies on projecting Toronto Metro rent prices, I encourage you to explore this phenomenon, as it holds significant importance.

Why Toronto Metro Market is Weakening?

Why did the Toronto Metro real estate market shift from tightening to weakening in May and continue to do so in June? While I cannot provide a definitive answer, I would like to share my thoughts on the possible cause. One popular explanation is linked to the recent rate hike by the Bank of Canada.

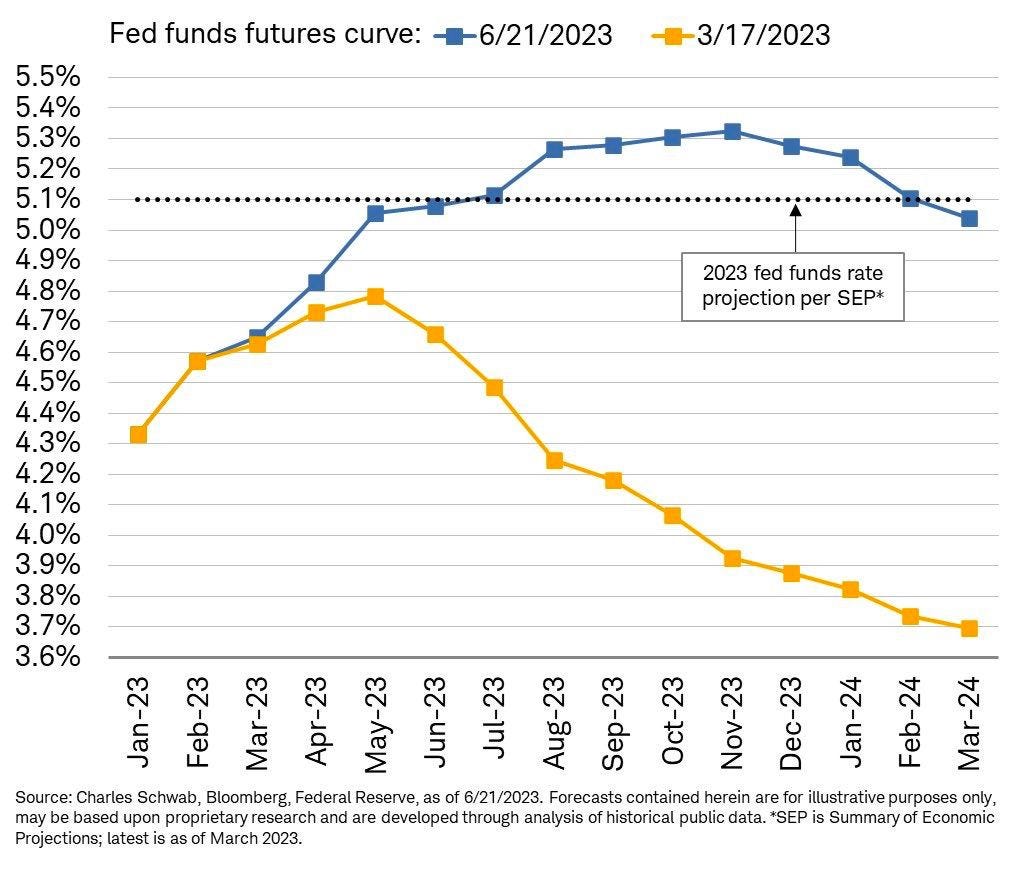

However, since the weakening began in May before the rate hike in June, it cannot solely account for the shift. Moreover, a 0.25% increase is not substantial. In my opinion, the rate hike is a consequence rather than the cause, and the underlying reason lies in stronger-than-expected economic data. This data has led to higher inflation expectations among both the Bank of Canada and the market. Here is an example of how market expectations for interest rates in the US changed since March this year.

Unfortunately, I do not have similar data for Canada, except for the one shared by Richard Dias. Although it may be slightly more challenging to interpret, it tells a similar story.

The market is gradually realizing that interest rates might remain elevated for longer than previously anticipated. This realization likely motivates some sellers in the Toronto Metro area to list their properties. Bond yields are also rising due to the same underlying reasons.

Population Growth

The most recent data for the first quarter of 2023 (labelled as Q2 2023 in the dataset) indicates that Canada's population has grown by over 1.2 million in the past year, which is nearly three times faster than the usual rate when compared as a percentage of the population.

Official data is lagging and leading indicators are so convincing that the new record wasn’t a surprise at all.

All these factors contribute to a “perfect storm” for population growth in Canada, leading to expectations of new records ahead. (link)

Furthermore, the significant time lag means that the same leading indicators are already pointing towards surpassing this new record when the population growth data is updated again in three months.

It is crucial to emphasize that out of the 1.2 million population growth, 734,040 individuals were a net increase of non-permanent residents.

This distinction is important because population growth is often incorrectly equated with immigration, leading to wrong conclusions. For instance, my recent Twitter poll revealed that approximately half of the respondents believed that the robust population growth coupled with a slowdown in new construction represents some form of an ultimate bull case for the housing market in the Toronto Metro area.

Undoubtedly, strong population growth is a significant factor, but I would like to highlight a few points that may be overlooked by those who selected the first two options. These points are based on my knowledge and experience, and you are welcome to disagree.

Population growth does not equal immigration. While it is reasonable to expect that many non-permanent residents will transition to permanent status, this remains speculative. By definition, it is also possible for temporary residents to leave Canada under certain conditions, a possibility that is often overlooked.

Household size is not a constant, but a variable that dynamically changes. According to the latest census, the household size in the Toronto CMA was 2.72. Let's consider a scenario where the unemployment rate rises, and individuals who have lost their jobs move back in with relatives or opt for co-living arrangements. As a result, household size increases from 2.72 to 2.83.

The calculated impact of this change on housing demand would be equivalent to removing approximately 190,000 people from the Toronto Metro, which exceeds the yearly population growth. Some people assume that household size is constant, therefore an estimate of housing shortages is constant as well, which is not the case.

A slowdown in new housing construction as a result of higher interest rates or falling home prices is a very typical market response. Regardless of that market response, housing corrections do happen.

Although the number new construction sales in Toronto Metro this year is relatively small, there are more than 100,000 housing units currently being constructed, which will eventually be completed. This amount accounts for three years’ worth of typical housing supply. Today’s decline in pre-sale activity should be compared to the population growth 4-5 years down the road and we couldn’t know in advance what it would look like.

While it is possible that the strong population growth coupled with a construction slowdown may lead to a tighter Toronto Metro real estate market in the future, it is important to note that there is no certainty in this outcome. Therefore, I would caution against the assessment of an "ultimate bull case."

Interest Rate Increases are Working

Despite the Bank of Canada resuming monetary policy tightening and the recent rise in inflation expectations, interest rate increases are working.

Savings rates and job vacancies are declining, insolvencies are increasing, and there has been a recent uptick in the unemployment rate.

While none of these indicators have reached alarming levels yet, the direction of change is pointing towards disinflationary effects. All inflation metrics are showing a downward trend.

There is a considerable amount of criticism directed towards the Bank of Canada for trying to combat global inflationary forces. However, when we consider the broader perspective, it becomes evident that global inflationary forces are being addressed through a global response, where the Bank of Canada plays an important role.

We might observe further increases in unemployment and insolvencies, resulting in more new listings entering the market. In fact, anecdotal evidence shared by Ben Rabidoux suggests that there is already a sudden surge in insolvencies.

I cannot determine the extent of Canadian households’ resilience, as even the market and policymakers consistently underestimate it. Therefore, I refrain from making predictions and instead, follow the incoming data. It seems reasonable to anticipate a weakening labour market and an increase in insolvencies.

Conclusions

The Toronto Metro real estate market significantly weakened in June. The increase in new listings and decline in sales contributed to a rise in active inventory and a deterioration of market balance indicators. As the market transitions from a tight state, it will take some time before any price declines become evident. While certain price metrics showed a decline in June and others displayed an increase, overall prices likely continued to grow compared to the previous month. If the current market dynamics persist, we should anticipate a balanced or even buyer's market as early as July. This would imply either flat prices or a decline.

In my perspective, the primary factor behind this market shift is the notable increase in future interest rate expectations. The market anticipates higher rates for longer, which is generally bad news for the real estate market. The increase in resale inventory is likely speculative at this stage, indicating that sellers are proactively listing their properties to either capture appreciation or avoid potential financial difficulties in the future. I am not aware of significant signs of forced selling where individuals are listing their properties because they have to. If you see that happening on significant scale, please let me know.

In my February 2023 newsletter, I correctly identified the rebound in the Toronto Metro market, stating:

“I would like to clarify that I don’t know what kind of rebound we are facing. Will it be a small uptick followed by a further market slowdown, or a medium/long-term market bottom? Setting aside speculation about the future, it is important to acknowledge that the market is turning, and if your view is bullish, this could be an opportunity.” - Mar 8, 2023 (link)

Today, the opposite is occurring, and while it is impossible to determine the extent of the market's weakening, similarly to February, it is essential to acknowledge that the market is once again undergoing a turning point, signalling the end of the bull market stretch observed in the Toronto Metro real estate market since February.

Furthermore, I would like to emphasize that the worst housing affordability since the 80s and investment attractiveness which I mention almost in every newsletter are crucially important. These fundamentals represent correction potential akin to the build-up of snow in the mountains. We cannot predict if or when an avalanche will occur, but it should not be surprising if it does.

Rent prices continue to rise but mostly align with historical patterns, which is remarkable given the explosive population growth in Canada. The country witnessed a new record with an annual increase of 1.2 million individuals, nearly three times faster than the usual rate. The majority of this growth is attributed to a net increase in non-permanent residents. While population growth is a strong fundamental and may make the real estate market appear bulletproof, I outlined certain risks to this view.

Analysis of macro data confirms that the interest rate increases are having an impact, with key indicators moving towards the disinflationary side. While none of the analyzed indicators have reached concerning levels, two of them warrant particular attention: unemployment and insolvencies. If either of these indicators continues to weaken, it may lead to forced selling by property owners and subsequently contribute to an increase in new listings in the market.